Abstract

Introduction

The popularity and use of online platforms to access housing have increased in recent years, with platforms having different ‘logics’, business models and socio-technical structures (Fields and Rogers, 2021). These platforms range from generalist websites offering a variety of goods and services including housing, such as Craigslist.org and Gumtree.com, to purposefully designed websites within the so-called ‘PropTech’ sector (Shaw, 2020) such as Zillow.com and Realestate.com.au, and the ubiquitous short-term rental market for residential tourism epitomised by Airbnb.com. Many of these platforms facilitate access to discounted accommodation, whereby regulatory requirements are bypassed or violated in return for lower rents (Gurran et al., 2023). The term ‘informal’ housing is often used to describe such accommodation, with reference to the wider ‘informal’ economy characterised by unregulated and sometimes illicit practices that take place in the shadow of government oversight (Ferreri and Sanyal, 2018). In relation to housing, informality refers to a situation where building, planning or rental regulations are avoided or contravened, and/or residents have fewer protections under such laws (Harris, 2018; Maalsen et al., 2022). Examples include dwellings that fail to meet construction or planning requirements, or tenures not covered by standard rental leases including shared housing arrangements characterised by more complex tenancy agreements and/or interpersonal relationships (Maalsen and Gurran, 2022). The increasing shortage of social and affordable housing supply and consequential demand for alternative arrangements make it important to interrogate the nature and role of informal markets as a supplementary source of accommodation within the wider system.

The article investigates this terrain by exploring the range of real estate platforms and their role in relation to low-cost and ‘informal’ rental housing supply in Sydney. We focus particularly on the lower end of the rental market: using an affordability benchmark of AU$325 per week 1 as an initial screen for non-standard dwellings or rental arrangements meeting criteria associated with informality. We ask what types of low-cost and informal rental markets are enabled and exposed by digital platforms, and how these markets intersect with the wider geographic distribution of rental accommodation and households in Sydney. Using a combination of web-scraped and manually collected datasets on rental listings advertised on four dominant housing related platforms during August 2020 – Realestate.com.au, Flatmates.com.au, Gumtree.com.au and Airbnb.com – we examine the scale, spatial distribution and nature of accommodation offered.

The structure of the article is as follows. First, we offer a brief overview of the literature on informal housing in relation to the increasingly pervasive role of online platforms in the housing market. Second, we introduce the case of Sydney and our research methods. We then present the results of our analysis in relation to the four dominant platforms for offering or seeking housing in Australia. Our findings reveal a complex and digitally enabled sector of the private rental system which ranges from higher-cost and quality short-term rental accommodation offered on platforms such as Airbnb, often targeting visitors or highly paid skilled migrants, through to forms of shared accommodation, secondary dwellings and substandard units advertised via different online platforms and offering various rental prices and tenure arrangements. Embedded within the wider housing stock and market, these various tenures and dwelling types may supplement more conventional rental supply, particularly during periods of high demand. The potential role in accommodating lower-income renters with limited alternatives makes it important to examine this digitally enabled sector of the rental market. By drawing together data from four platforms in Sydney, the study extends previous research on informal and online rental markets which focused on single data sources (Boeing and Waddell, 2017; Harten et al., 2021). Overall, the study contributes to an emerging body of research on the intersections between digital platforms and changing market practices, which are at once enabling and revealing hidden segments of the housing system.

Informal housing, digital platforms and the rental market

A small but growing body of literature recognises informal housing practices and markets in so-called Global North countries (Harris, 2018; Mendez, 2017; Shrestha et al., 2021). A key ambiguity is the role of the state in both defining informality and also creating the conditions in which informality arises, by exercising the regulatory power to define and enforce housing laws (Banks et al., 2020; Roy, 2005; Schiller and Raco, 2021). The state’s failure to address unmet housing needs also creates demand for informal housing alternatives which historically have included unauthorised secondary dwellings, substandard single room rental accommodation in former hotels, loosely regulated ‘trailer’ parks and unpermitted additions and subdivisions within dwellings (Durst and Wegmann, 2017; Mukhija and Loukaitou-Sideris, 2014). More recently, researchers have considered unscrupulous room and shared room rental operators as well as short-term Airbnb-style rentals to be examples of digitally enabled informal rental accommodation (Lombard, 2019; Nasreen and Ruming, 2021; Shrestha and Gurran, 2024). All of these examples share a failure to comply with established laws, or offer residents fewer protections against these regulations (Harris, 2018), whether these violations relate to the physical structure of the dwelling, the nature of the tenancy or both (Shrestha et al., 2021).

It is important to distinguish between the notion of housing ‘precarity’– the insecurity experienced by lower-income earners whose housing tenure may be at risk because of their limited financial resources (Lombard, 2021) – and ‘informality’, which refers specifically to housing that does not follow standard building and/or tenure regulations or that offers lower protection for residents against these regulations and may be produced by actors across the housing system including property owners and landlords (Harris, 2018). In making this distinction, it is important to note that conditions which give rise to rental precarity (i.e. a shortage of affordable and appropriate accommodation) also contribute to a market for alternative options, including forms of informal rental supply. Thus, informality in the 21st century may emerge as a response to unmet housing need (Wetzstein, 2017), reflecting structural problems associated with state failures (Schiller and Raco, 2021). But it may also be a strategy for ‘elite’ groups to profit by avoiding the regulatory costs associated with formal construction or rental supply (Banks et al., 2020). In this sense, informality is not limited to need-based strategies adopted by the urban poor but may also be carried out for profit (Devlin, 2018). These shadow practices and markets occur within the formal housing stock, intersecting with planning and property laws to create what Roy describes as ‘a distinctive type of market where affordability accrues through constraints or absence of formal planning and regulation’ (Roy, 2005: 149).

In Global North cities, the hidden and ‘deliberately concealed’ nature of informal housing presents challenges for researchers and practitioners where the exposure of such practices may result in subsequent punitive regulatory measures, for instance demolition orders. Even when the target is unscrupulous providers, regulation or enforcement actions may lead to the loss of accommodation, worsening the situation for residents (Maalsen et al., 2022). Consequently, researchers emphasise that the structural disadvantages that give rise to unmet housing need must be identified and addressed before progressing interventions which may deplete the supply of informal accommodation (Recio and Shafique, 2022).

Platform-enabled housing informality

Digital real estate platforms that allow users to access global housing markets via powerful digital tools have been described as occupying a critical nexus between digitisation and neoliberalism (Ferreri and Sanyal, 2018). With housing markets highly segmented according to the location, amenities, cost and tenure of properties, the capacity for geodata-enabled search engines to connect potential users (buyers, sellers, renters, sharers, etc.) is transformative. By reducing the usual ‘transaction costs’ associated with searching for property, and extending market coverage beyond local geographies (Fields and Rogers, 2021), many real estate platforms have arguably exacerbated the commodification of housing as a global, financialised asset (Shrestha et al., 2023). They also facilitate new socio-technical relationships, particularly between people offering or seeking accommodation (Nasreen and Ruming, 2022; Parkinson et al., 2018). The rising importance of online platforms, replacing or resituating ‘real-life’ social networks in digital space, has been found to be important for marginalised renters often unable to access the formal rental market (Parkinson et al., 2018). Traditionally those excluded from the formal rental market would rely on social networks and their capacity to search potential locations for shared home vacancies, boarding house rooms or ‘lodgings’, but digital platforms offer powerful search tools to connect people offering or seeking accommodation at a time of escalating housing crisis (Shrestha et al., 2023).

A small body of literature has begun to consider the intersections between the digitally enabled informal rental sector and the wider market. There is the potential for informal rental providers to relieve pressures in the formal system by creating new supply within existing properties. However, the potential to add an additional rental unit (such as a secondary dwelling), or to yield a higher rental income by renting properties to multiple tenants by the room rather than as a single dwelling, may also have inflationary impacts on rents or prices (Zhang and Gurran, 2021). Likewise, short-term Airbnb-style rental accommodation can create gentrification pressures by depleting the rental stock and converting it to short-term tourist accommodation (Horn and Merante, 2017; Wachsmuth and Weisler, 2018). At the same time, ‘sharing’ a primary residence with tourists via platforms such as Airbnb, while the ‘host’ remains living onsite, can be a strategy for cost-burdened renters or home-owners to gain some income relief (Gurran and Phibbs, 2017).

However, rental vacancies advertised via digital platforms may have a higher risk of exposing potential tenants to unsafe or insecure living situations. Landlords or their agents may present misleading information about the quality or cost of residential properties; indeed, in a study of shared dwelling advertisements in Shanghai, Harten et al. (2021) found that listings were used more to lure potential tenants rather than to communicate accurate information about particular accommodation vacancies. In this sense, these platforms facilitate access to an alternative and informal rental supply for those in housing need but also enable a market in accommodation of lower and sometimes substandard amenities as well as reduced legal protections associated with rental tenures (Maalsen et al., 2022).

The ability to market such accommodation online via digital platforms makes it easier for providers to evade local planning, building and rental laws, as has been widely documented in relation to the Airbnb-style short-term rental sector (Ferreri and Sanyal, 2018; Gilbert and Gurran, 2017). With digital platforms not responsible for listings accuracy, landlords are able to hide their identities with fake names and disguise the exact location of property in order to evade regulators (Nasreen and Ruming, 2022). Ferreri and Sanyal (2022: 1035) refer to ‘digital informalisation’ of housing occurring ‘in the shadow of formal regulations’, whereby ‘legal, illegal, legitimate, illegitimate, authorised and unauthorised’ practices are in a dynamic relationship (Ferreri and Sanyal, 2022: 1038). Challenging simplistic associations between informality and poverty, they argue that digital platforms and the informal economic activities they enable engender ‘possibilities that are ripe for exploitation and profit-making’, for instance through unregulated private letting and sub-letting practices ‘in the interstices and under the radar of formal, lawful housing’ (Ferreri and Sanyal, 2022: 1039). Such digitally enabled practices both exploit and can potentially exacerbate rental precarity and socio-spatial inequality.

In countries such as Australia, where regulatory enforcement of the private rental sector depends on tenants themselves exercising their rights via complaint to a legal tribunal, there are additional risks that platforms make it easier for landlords or their agents to market substandard accommodation (Shrestha and Gurran, 2024). Combined with a lack of alternative low-cost accommodation, this lack of proactive enforcement of rental standards has meant that tenants occupying informal, unsafe and overcrowded housing in Sydney are reluctant to complain against their landlords for fear of eviction (Nasreen and Ruming, 2021). It is within this socio-digital context that a market for informal accommodation has evolved in Sydney.

Investigating informal and low-cost housing in Sydney

Sydney, Australia’s largest city, has a population of over five million people residing across a metropolitan region spanning over 12,000 km2 (ABS, 2022). Over the past decade, rates of homeownership have fallen steadily, with almost a third of households (35.9%) renting in 2021 (ABS, 2022). Sydney’s rental market is highly competitive and expensive, where vacancy rates often fall below 2% and 35.3% of all renters paid more than 30% of their income on housing at the time of the 2021 census, reflecting chronic affordability pressures (ABS, 2022). As a broad indicator of the extent of shared housing across the city, 4.2% of households identified as a ‘group household’ of unrelated adults living together, with higher proportions of such households in inner-city localities (10.8% in Sydney’s Inner South) (ABS, 2022). Geographically, Sydney’s Inner City and Eastern Suburbs are focal areas for employment, education and tourist attractions, such as the famed Sydney Harbour and Bondi Beach. Although Sydney is characterised by pockets of socio-economic advantage and disadvantage across the metropolitan region, household incomes in the western and southwestern areas of the city are relatively lower (Easthope et al., 2018).

Australia’s private rental sector

Like comparable nations such as the UK or USA, Australia’s private rental sector is dominated by small ‘buy to let’ landlords, who typically own one or two dwellings in the form of single homes (Yanotti, 2017). The six states and two self-governing territories regulate the private rental sector, administering laws governing the private rental market, but there are broad similarities across all jurisdictions. Professional real estate agents manage a majority of rental properties, with residential tenancy leases usually offered on a six- to 12-month basis, following which time landlords are able to end the lease of the property. Rents are determined by the market, and rent control measures such as rent caps are largely absent, operating to limit the frequency of rental increases only. In New South Wales (NSW), the Residential Tenancy Act (RTA) 2010 establishes the minimum period of tenure, property standards, rental and bond collection and dispute resolution. Formal residential tenancy leases are usually administered by property agents operating on behalf of landlords. These leases offer between six and 12 months of security of tenure; prevent landlords from entering the property without notice; and establish obligations for property standards and maintenance. When share arrangements are established between tenants, residents may be named on the lease as co-tenants, or a head tenant may declare that they have entered into an arrangement with sub-tenants, provided that they have the approval of landlords. However, in many shared houses, not all tenants are named on the tenancy agreement, especially where head tenants are allowing new tenants without the consent of the landlord (Nasreen and Ruming, 2021). Thus, tenants who do not have written agreement from the head tenants and/or landlords are excluded from the protection of the RTA 2010.

Other types of rental arrangements apply to registered ‘Boarding Houses’, which offer rooms for rent, typically for shorter tenancy periods under the Boarding House Act (BHA) 2012. The same law covers ‘lodgers’ who rent rooms in a private house. Boarders and lodgers have fewer rights than tenants, and due to the informal nature of the agreements by which many people access such accommodation without an intermediary agent or residential tenancy lease, they are often unaware of any entitlements that do apply. Low-income tenants without a secure income or the ability to pay four weeks’ rent as an advance bond, or people without rental references such as recent migrants, find it particularly difficult to access the formal rental market and are more likely to enter the informal sector (Nasreen and Ruming, 2021). While rents may be lower in this sector, landlords may opt for these informal arrangements to bypass rental tenancy regulations or to avoid paying additional income tax or agent fees (Alam et al., 2022).

Residential planning and construction rules

Australia’s legal regime for housing construction is administered by the states and territories, each of which enacts its own land use planning laws (covering zoning and development controls) and formally subscribes to a national construction code (containing minimum building and construction standards). In Sydney, the state’s NSW Environmental Planning and Assessment Act (EPAA) 1979 sets out the parameters for local planning controls, including rules around residential dwellings. In 2009, the state enacted a state-wide code to encourage secondary dwellings on residential sites, overriding any local planning rules which may have otherwise been in place (Shrestha and Gurran, 2024). This resulted in a significant increase in the number of secondary dwellings in Sydney (Troy et al., 2018). At the same time, local councils in some parts of Sydney reported a significant problem with unpermitted and non-compliant secondary dwellings, which are being offered in the rental market alongside other types of substandard and unauthorised forms of accommodation (Shrestha and Gurran, 2024). As with residential tenancy regulations, the state lacks a proactive enforcement regime in the private building sector. However, even when local enforcement officers become aware of illegal dwellings, they are often reluctant to enforce regulations if that would result in a residential tenancy eviction, within a broader context of unmet housing need (Gurran et al., 2021).

Methods

To investigate the informal rental submarket in Sydney, we examined listings on four platforms: Realestate.com.au, Gumtree.com.au, Flatmates.com.au and Airbnb.com (see Table 1). These platforms were selected because they dominate market share and because they each target different segments of the informal rental market (informal dwellings, tenures, shared housing and short-term rentals), avoiding the risk of duplicate advertisements. Each platform was then examined in detail to explore the types of housing supplied in order to delineate search criteria on the basis of: (a) rental cost, including low-cost housing with weekly rent up to AU$325; (b) informal tenure or occupancy arrangements (such as sharing or renting from owners with negotiated tenancy requirements); and (c) non-standard or informal dwelling structures such as secondary dwellings, boarding house rooms, subdivided apartments and so on.

Summary of platforms and data.

Data from all platforms were collected for the month of August 2020 at the suburb 2 level (for higher accuracy at a smaller scale), and then summed at the sub-region (Statistical Area Level 4 (SA4)) level for geographic comparative analysis. SA4 boundaries represent labour markets and the functional areas, and associated socio-economic variation across Sydney. We calculated the total volume of informal housing advertisements relative to the rental stock enumerated by 2020 data between the Australian Bureau of Statistics (ABS) Census data 2016 and 2021, and market vacancy rates (enumerated by commercial supplier ‘SQM’ (Supplier Quality Management) based on total rental listings). We drew the data together for benchmarking against established housing indicators (stock of rental units, dwelling structures, tenure type, shared households) for the broader rental market.

The selected period (August 2020) was somewhat atypical in Sydney’s rental housing market, with a potential increase in demand for new rental tenancies triggered by the ending of COVID-19 lockdown restrictions and national border closures. Demand for short-term rental accommodation was thought to be largely dormant during the period as well, due to the lack of international tourists (Buckle et al., 2020), relieving some of the rental pressure in Sydney. Overall, Sydney experienced the highest rental vacancy rate in May 2020 (4.3%), although this fell to 3.7% in August 2020, reflecting an easing of lockdown restrictions (SQM Research, 2023). However, Australia’s housing affordability pressures remained, with prices rising to all-time highs, driven by low interest rates and government grants for home purchases and construction. As our data show, demand and supply of informal rental accommodation continued in Sydney throughout this period, despite the general easing of supply in the formal sector.

The range of platforms examined necessitated a mixed-methods approach to data collection and analysis. While web-scraped data were available for Flatmates.com.au and Airbnb.com platforms, listings on Gumtree.com.au and Realestate.com.au required manual data collection, review and analysis. This distinction was important as terminology in user-supplied information was inconsistent across each platform. For instance, an advertisement for a ‘house’ in Realestate.com.au could refer to a detached dwelling, a ‘granny flat’ or even a room in a shared house. Similarly, in Gumtree.com.au various terms were used to describe tenure arrangements and the types of accommodation advertised (Table 1). Consequently, our methods for collecting listing data in these two platforms involved systematic rental property searches across Sydney. The research team also undertook text description and visual analysis of listing photographs to aid in classifying the accommodation from these two platforms (Realestate.com.au and Gumtree.com.au). Visual analysis of Realestate.com listings conducted by our research assistants (each of whom had professional planning qualifications) enabled us to distinguish whether properties appeared compliant, or non-compliant, with building and safety standards.

The platform Realestate.com.au (hereafter Realestate) primarily advertises properties which are managed by professional real estate agents. However, it was observed that low-cost listings (weekly rents up to AU$325) include shared occupancies and non-standard dwellings such as boarding houses and secondary dwellings. A total of 2108 Realestate listings matched our study criteria on low-cost and informal housing listings. Gumtree.com.au (hereafter Gumtree) ‘property for rent’ listings for whole dwellings are mostly advertised by landlords directly (i.e. property owners/head lessees, including those living on the premises themselves), rather than professional real estate agents. Direct arrangements between a landlord and tenant require a level of negotiation and ongoing communication, and are often characterised by informal agreements (Alam et al., 2022). These ‘property for rent’ listings (all rental costs) on Gumtree (

Shared accommodation listings on Flatmates.com.au (hereafter Flatmates) included user-supplied data on the location and characteristics of the shared dwelling, the duration of the vacancy and the rental cost. In addition to these data categories, listings contain free-text descriptions often about the household offering a vacancy, such as the reasons for seeking tenants or offering accommodation. Both private rooms and shared rooms are advertised on Flatmates. As shared tenancies are typically regarded as informal because of the negotiated tenancy requirements, reduced regulatory protections as well as compromised amenities, the entire Flatmates data (

Airbnb data were accessed via the independent data source Insideairbnb.com, which has been used in a growing number of studies across the world. Our rationale for analysing this dataset was twofold. We wanted first to establish the number of residential homes used as informal tourism accommodation via the Airbnb platform, and second to understand the potential implications of this informal, short-term rental market for the supply of, and demand for, permanent rental accommodation more widely. Thus, key data points include both the total number of Airbnb listings and the composition of properties (whole ‘un-hosted’ homes versus ‘hosted’ rooms or shared rooms), and the proportion of whole dwellings which appear to be permanently available short-term rental accommodation. Combined, these data allow us to distinguish between informal tourism activities which deplete permanent rental supply – properties available more than 90 nights a year – and those which may help local residents gain additional income by temporarily hosting fee-paying visitors.

While GIS mapping shows the spatial concentration of different informal housing types, the regression analysis tests and verifies location-specific characteristics. The dependent variable is informal listings relative to the total rental housing stock at the suburb level, ensuring a consistent measure across Sydney despite variations in residential density overall and rental households in particular. Location-specific variables (see Table 2) included the overall structure of dwelling stock (with the prevailing residential dwelling stock potentially influencing the types of informal dwellings likely to be produced at the suburb level) and socio-economic characteristics of the population (income level, levels of housing affordability, migration). These three indicators – income, housing affordability ratio (households paying over 30% of their income on rent or mortgage) and the proportion of the population who had migrated to Australia in the past decades – were tested as possible drivers of demand for informal rental accommodation. We further created geographic control variables (dummy variables) for sub-regional variation with spatial fixed effects through the SA4 boundaries to reduce third-variable bias (Hardy and Reynolds, 2004), considering other multiple explanatory variables (potential confounders) related to geographical differences that might affect the results.

ABS census 2021 TableBuilder variables at the suburb level.

Four regression models are presented for each informal rental platform. We used multiple linear regression with a stepwise variable selection process (criteria: probability-of-

Understanding Sydney’s informal and low-cost rental supply

We now present our analysis of data from each platform in turn, before comparing rental costs and supply advertised across each site in relation to Sydney’s wider rental market and socio-spatial dynamics across areas.

Low-cost and informal housing on the Realestate platform

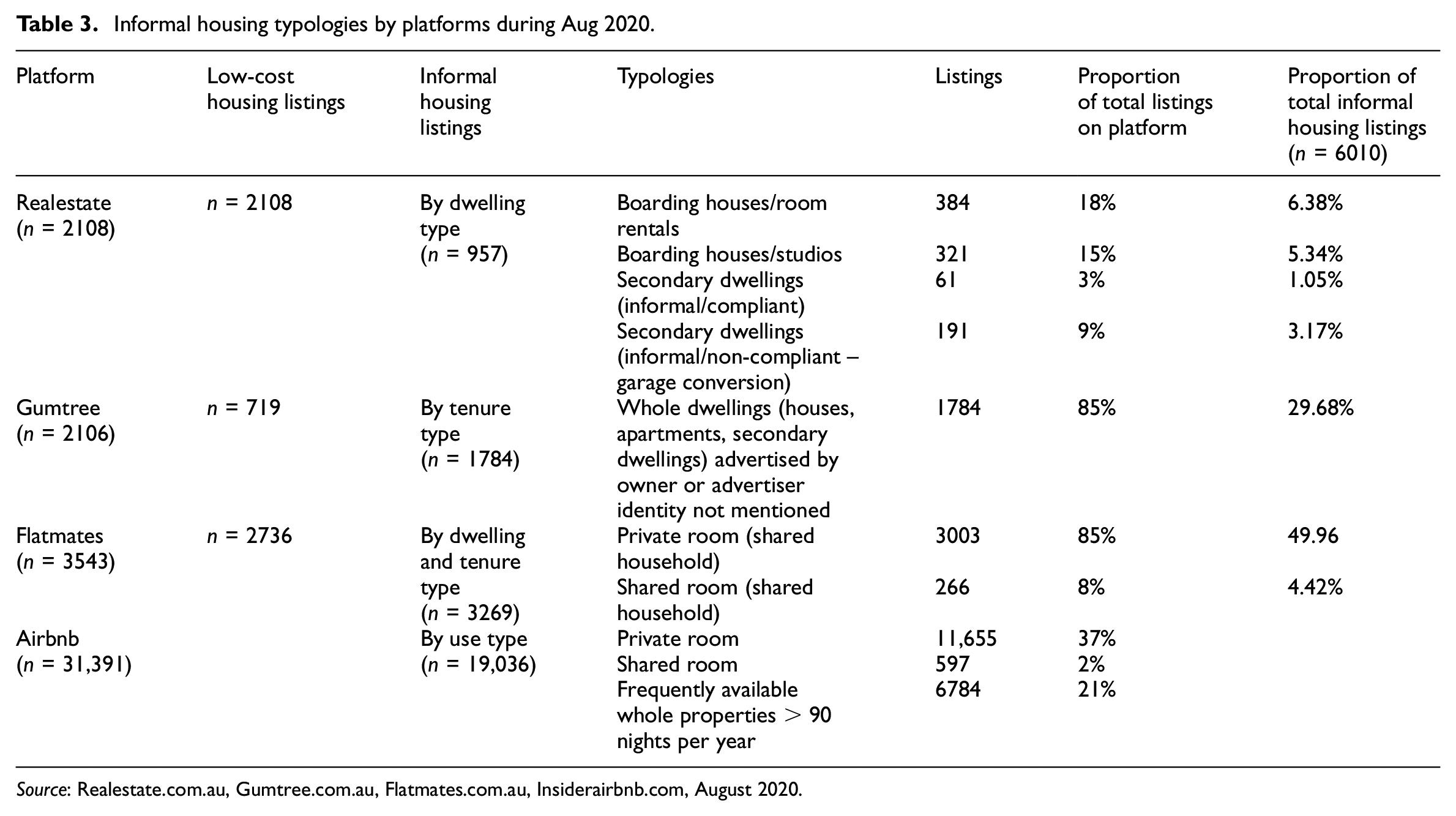

Our analysis of data from the Realestate platform revealed more than 2000 properties listed at weekly rents of up to AU$325 in Sydney. Of these, 22% were advertised for a rental cost of up to AU$250, and the balance were advertised for between AU$251 and AU$325 per week (Figure 1). We identified ‘boarding houses’ (either room rentals or studios), ‘secondary dwellings’ and complete dwelling units and further categorised them according to regulatory criteria (applying to newly constructed boarding houses and secondary dwellings) and the nature of occupancy. This analysis revealed that almost half of Sydney’s lower-cost Realestate listings (45%) consisted of potential informal accommodation types, comprising 384 boarding house room rentals, 321 newer self-contained boarding house rooms and 252 secondary dwellings (Table 3).

Informal and low-cost housing listings by platforms during August 2020.

Informal housing typologies by platforms during Aug 2020.

The majority of lower-cost listings in the Inner City areas indicated informality, and of these boarding houses dominated supply (91%). Overall, boarding houses (room rentals and studios) made up 33% of advertised low-cost rental listings on Realestate (see Table 3). Despite the NSW state policy establishing a legal pathway for secondary dwelling construction, our data found that such units accounted for only 252 (approximately 12%) of Sydney’s total lower-cost rental supply advertised on the Realestate platform. The majority of these (

Low-cost and informal housing on the Gumtree platform

Of the total number of whole dwellings advertised (2106) on Gumtree, 15% were listed by real estate agents (and were excluded from our analysis), while the majority were identified as for ‘rent by the owner’ or via an unspecified arrangement. These listings (

Our visual analysis of listings photographs on the Gumtree platform revealed that around 30% of listings classified as a secondary dwelling of some type, while the balance were whole homes or rooms within homes. The photographic analysis also revealed substandard dwelling conditions (e.g. lack of windows) or inadequate construction materials (e.g. lack of insulation, exposed pipes and wiring).

Low-cost and informal housing on the Flatmates platform

Of the total 3543 shared housing vacancies listed on Flatmates, more than half were clustered in the City and Inner South, Eastern and Western suburbs. This is consistent with ABS census data on the geographic distribution of group households (Figure 2). Shared housing listings on Flatmates counted for 4.6% of Sydney’s group households. As expected, shared housing accommodation tends to be lower in cost than self-contained rental units and 48% of listings were offered for rents of up to AU$250 per week (concentrated primarily in lower-value housing markets of the western suburbs). A further 29% of listings were advertised for between AU$251 and AU$325 per week in Sydney, leaving around a fifth of shared vacancies priced beyond the affordability threshold of AU$325 per week (Figure 1). Overall, low-cost housing made up almost 84% of the informal shared housing listings on Flatmates. Most Flatmates listings in our data were for private rooms within an existing shared house (85%). However, 266 (8%) of listings were for shared rooms.

Informal housing typologies via three platforms (Realestate, Gumtree and Flatmates) versus related ABS variables in Sydney.

Supply of short-term accommodation on the Airbnb platform

If shared housing on the Flatmates platform increases supply, the Airbnb platform depletes it; yet short-term rental listings on Airbnb during August 2020 (

Of particular concern from the standpoint of rental housing supply is the 6784 (21%) entire homes that appear to be available for more than 90 nights (three months) per year. These homes are likely to have been removed from the permanent rental market and therefore exacerbate supply pressures, with flow-on impacts for rental price (Wachsmuth and Weisler, 2018). Notably, border restrictions during COVID-19 lockdown and the lack of international tourists appeared to motivate some landlords to withdraw properties from sites such as Airbnb (Buckle et al., 2020) so our data probably underestimate the quantity of short-term rental accommodation in Sydney.

Understanding informal housing supply relative to socio-spatial dynamics

The analysis reveals that there were more than 6000 informal housing listings (

Notably, the supply of informal housing was highest in the City and Inner South region, equating to almost 1.9% of the enumerated rented dwelling stock in these well-located areas. Parramatta and the Inner South West regions also had relatively higher volumes of potential informal and low-cost supply, whereas the Eastern suburbs exhibited a high volume of informal housing listings but few of these offered lower-cost opportunities in this affluent beachside region.

The composition of informal housing types exhibits clear variations across the different locations of Sydney (Figure 2). For example, in the City and Inner South, the informal supply is dominated by shared houses, in comparison to the Inner South West and Parramatta where whole dwellings rented directly by landlords are prevalent. Further, the number of secondary dwellings listings is higher in the South West, Blacktown and Parramatta than other SA4s in Sydney. In turn, these spatial differences in the informal housing typology relate to statistically significant demographic and dwelling characteristics across Sydney.

Table 4 shows the regression model summaries, including predictor significance, for the informal housing rate in the rental housing stock for different informal housing types at suburb-level analysis. Model 1 shows that the rate of boarding houses in the rental housing stock occurs where there are more ‘townhouses’ (i.e. attached dwellings) in the dwelling structure (

Regression models and coefficients values for statistically significant variables for informal housing types in rental housing stock.

The rate of secondary dwellings (Model 2) is negatively associated with an overall excess of bedrooms in the housing stock (

Overall, the total ‘rate of informal tenure listings’ in the rental stock (Model 3) is positively associated with shared households (‘renting with a person not in the same household’) (

The dependent variable ‘shared houses rate in rental housing stock’ (Model 4) is positively associated with predictor variable group households (

Discussion

The data presented here support previous research which asserts that Australia’s informal rental markets are probably targeting lower-income and marginalised groups with limited alternative housing options, who are prepared to trade off tenancy rights, housing amenities (including privacy) and/or tenure security (Gurran et al., 2021). The findings in this study, which point to a significant supply of informal rental housing, not all of which is being offered at an affordable price point, suggest that residential landlords may be capitalising on the wider lack of affordable and social housing supply in Sydney by offering informal rentals which are at a lower cost than prevailing ‘formal’ offerings but still expensive for lower-income renters. Not only are many listings priced above the affordability threshold of AU$325 per week, especially listings on the Gumtree platform, but, as highlighted by earlier research (Nasreen and Ruming, 2021), properties which may be technically ‘affordable’ to lower-income earners are often inappropriate due to substandard building quality, exposing residents to health and safety risks.

Our data confirm that the shortage of affordable vacancies within the formal rental market appears to be exacerbated by the appropriation of residential homes to short-term tourist accommodation via Airbnb. Ironically, the long-term informal rental housing supplied through three main platforms (Realestate, Gumtree and Flatmates) appeared equivalent (1%) to frequently available whole properties removed from Sydney’s permanent rental housing market through Airbnb. The supply of shared accommodation (private and shared rooms) is unique within the housing market, as shared housing can be understood to create, rather than exhaust, vacancies in the housing stock (Gurran et al., 2023). Thus, our data indicate that the shared housing sector is making a significant contribution to rental supply in Sydney’s tight rental market. Nonetheless, unlike the institutionalised supply of shared housing emerging in Europe, such as in Amsterdam (Uyttebrouck et al., 2020), our study raises concerns about the operation of an unregulated private rental market in shared accommodation without proper communal facilities for multiple adults living together. That this supply continued during the study period under the COVID-19 pandemic conditions only underscores the demand for lower-cost accommodation in Sydney, which overrode concerns around disease transmission and persisted despite the closure of international borders reducing the numbers of international students known to occupy shared housing.

Our platform data reveal that informal accommodation is occupying distinct segments of the private rental sector. Notably, each of the platforms contributes a different type of accommodation offering (related to their distinct business models and targeted users). While Flatmates dominated informal shared housing listings, making up 54% of total informal housing stock, it is important to recognise that this communal accommodation (private and shared rooms) is more attainable for young singles and may not serve the housing needs of other groups adequately, such as parents with children (due to caring responsibilities) and (older) people with a disability (Gurran et al., 2023). The Gumtree platform dominated the informal tenure listings of self-contained dwellings, making up 30% of informal housing stock, however these were typically priced beyond the affordability threshold for low-income households. Lower-cost informal housing such as boarding house room rentals, studios and secondary dwellings advertised on Realestate may be technically affordable and potentially suitable for a range of small household types; however, the need to supply a rental history and bond to qualify for a formal leasehold agreement may present some barriers to lower-income earners seeking to access accommodation via Realestate.

The spatial concentration of informal housing listings appears to follow distinct patterns by housing type and/or platforms across Sydney, relating to statistically significant demographic and dwelling characteristics while indicating data reliability. The regression results showing how boarding house listings are positively associated with lone-person households, shared housing listings with group households and informal tenure dwellings with tertiary education students indicate a consistent pattern and relationship between different types of housing listings on platforms and specific dwelling and household typologies (as known from ABS data) across Sydney. Overall, our data show that digital platforms have enabled a sophisticated and segmented informal rental submarket to emerge within Sydney’s formal housing market (Shrestha et al., 2023), offering a critical and supplementary source of rental supply.

However, questions remain about the appropriateness, quality and cost of this supplementary source of accommodation. As observed in a parallel study of the informal rental market in Shanghai (Harten et al., 2021), often the platform-mediated communication between potential landlord and tenant makes it difficult for people to ascertain exactly what type of accommodation is being offered, by whom and under what type of rental arrangement, whether by other residents in a shared household, an external landlord or real estate agent, a ‘head tenant’ acting on behalf of a third party or a resident owner occupier. Our dataset exposed unexpected intersections between these dwelling types, tenures and providers, including the prevalence of professional property agents on the Realestate platform advertising formal rental leases for potentially informal housing types, such as secondary dwellings, boarding houses and room rentals.

Conclusion

This study contributes to understanding the nature and scale of platform-enabled informal housing markets within the wider housing system. It is necessary to identify and understand this sector of the housing system in order to improve the quality and security of low-cost housing supply. With Sydney as a particular case study, our analysis shows the depth and differentiation of affordable and informal housing arrangements within an expensive and constrained private rental market. In revealing the different segments of the informal housing market as defined by accommodation types, tenure and occupancy arrangements, cost and location, we show the significance of the sector as a source of lower-cost or alternative accommodation for those facing affordability pressures and/or access barriers to the formal rental market. The study findings imply that informal markets are playing an important role in accommodating lower-income earners who have few alternatives but at the same time are exposing them to health and safety risks associated with poor-quality dwellings and insecure tenures.

Our research has also shown that digital platforms can be used by housing researchers and policy makers to monitor and respond to unmet housing need, while proactively enforcing standards across the private rental sector. In exposing the scale and nature of Sydney’s informal rental market, the policy opportunity is to respond by developing strategies to increase the formal supply of low-cost rental accommodation suited to different household types. Similarly, regulating the short-term rental sector would prevent further loss of supply and may over time return properties to the permanent market. Sustained investment in social and affordable housing combined with other forms of state assistance to reduce the vulnerability of low-income renters will be critical to reducing dependence on precarious and substandard housing without regulating out genuinely flexible housing opportunities which can supplement formal rental supply.

Supplemental Material

sj-docx-1-usj-10.1177_00420980241262227 – Supplemental material for Supplementary rental supply? The digital market for low-cost and informal housing in Sydney, Australia

Supplemental material, sj-docx-1-usj-10.1177_00420980241262227 for Supplementary rental supply? The digital market for low-cost and informal housing in Sydney, Australia by Zahra Nasreen, Nicole Gurran and Pranita Shrestha in Urban Studies

Footnotes

Declaration of conflicting interests

Funding

ORCID iDs

Supplemental material

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.