Abstract

Introduction

In this paper, we examine how client firms’ managerial ability influences audit outcomes. Management competencies are crucial in today’s talent market as they shape corporate policies, strategies, and overall outcomes (Bonsall et al., 2017), as well as influence the corporate information environment, which is central to public trust and credibility. A complete understanding of the accounting information environment requires investigating managerial idiosyncrasies, the “tone at the top” (Wells, 2020), and the auditors’ assessment of clients’ risk structures (Kizirian et al., 2005). Policymakers, such as the Public Company Accounting Oversight Board (PCAOB), underscore the significance of auditors’ assessments of client firms’ leadership structures, processes, and communications. Such scrutiny gauges how the “tone at the top” signals commitment to audit quality and performance. 1 In corporate settings, auditors are critical in ensuring that financial statements conform to Generally Accepted Accounting Principles (GAAP) in the US. Therefore, auditor assessments and opinions about managerial judgments and estimates are critical for audit outcomes (Wells, 2020).

Audit outcomes reflect how auditors evaluate the quality of a client firm’s information environment and risk structure in response to audit risks (e.g., recommending restatements for material inaccuracies and issuing opinions on internal controls) and final audit outcomes (e.g., audit fees, audit effort measured by audit report lag, and going-concern opinions). The empirical evidence on the impact of managerial skills and talent on audit outcomes is largely inconclusive and limited to audit fees and audit report lags. Therefore, we seek to provide a comprehensive understanding of whether and how managerial ability impacts both audit risk outcomes and final audit outcomes.

To establish a link between managerial ability and audit outcomes, our framework puts forth two opposing views that explain the potential impact of high-ability managers on audit outcomes. We argue that client firms managed by high-ability managers are more likely to achieve favorable audit outcomes, characterized by fewer financial restatements, reduced likelihood of adverse opinions on internal controls, lower audit fees, 2 shorter audit report lags, and a lower probability of receiving going-concern opinions (hereafter collectively referred to as “favorable audit outcomes”) for two reasons. First, high-ability managers have extensive knowledge, expertise, and a deep understanding of their business operations and macroeconomic conditions. This enables them to exercise better judgment, make precise estimations of the firm’s current earnings, and forecast future cash flows accurately. Consequently, they enhance the overall information quality within the firm (Baik et al., 2018; Demerjian et al., 2013; Wells, 2020).

Second, a capable management team is likely to enhance the auditors’ assessment of client risk by providing credible sources of information and evidence (Kizirian et al., 2005), strengthening internal controls (Judd et al., 2017), and mitigating liquidity and financial distress risks (Krishnan & Wang, 2015). Consequently, firms with superior managerial ability will tend to facilitate audit planning processes and lessen audit engagements. Overall, we argue that more able management teams will significantly contribute to favorable audit outcomes by raising the caliber of the client firm’s information environment and positively shaping the auditors’ assessment of client risk through improved internal controls, enhanced evidence credibility, and reduced liquidity and financial distress risk.

Conversely, high-ability managers’ significant influence over corporate decision-making and resource allocations may lead to managerial entrenchment and opportunistic behavior (Demerjian et al., 2020) like misuse of corporate resources, over-investment, and over-optimistic estimations of project cash flows (Chen et al., 2021). They may also engage in inappropriate accounting practices to maximize their personal benefit. For instance, high-ability managers who have gained significant power and become entrenched might involve themselves in unethical accounting practices to conceal critical firm-specific information (Koester et al., 2017), and rely on more subjective estimates of discretionary accruals or opportunistic earnings management (Gul et al., 2003). This would ultimately lead to a poor-quality information environment, requiring auditors to exercise greater prudence and professional skepticism (Jha & Chen, 2015), which raises the audit engagement risk, the number of inherent risk assessments, and the audit fees (Gul et al., 2003).

To empirically examine these two competing claims, we use a large sample of 35,252 firm-year observations from 3987 publicly listed US firms spanning 2000 to 2018. To capture the role of managerial ability, we use the measure developed by Demerjian et al. (2012), which evaluates how effectively managers translate corporate inputs into outputs compared to their industry peers. They are deemed exceptionally capable, for instance, if they generate more substantial revenue from a given level of resources. Across various audit outcomes, our analysis reliably shows that higher-ability managers are associated with fewer financial restatements, fewer internal control issues, reduced audit fees, shorter audit report lags, and a reduced likelihood of receiving a going-concern opinion. The base result is robust to various econometric specifications, subsamples, and alternative measures of high ability in management.

Despite strong evidence of the links between managerial ability and audit outcomes, there is the possibility of endogeneity limiting our inferences. Such concerns include potentially omitted factors, self-selection bias, and reverse causality. To alleviate these, we employ several identification strategies. First, we reestimate the association between managers’ ability and audit outcomes using firm-fixed effects, which helps us mitigate the issue of unobservable firm characteristics causing time-invariant omitted-variable bias. Second, we adopt an instrumental variable approach to address the heteroskedastic errors from unobserved common factors, as in Lewbel (2012). Third, we accept that self-selection bias could occur whereby high-ability managers tend to choose to work for firms known for having fewer restatements, fewer adverse opinions on internal controls, lower audit fees, less audit effort, and fewer going-concern opinions. Thus, to address such endogeneity concerns, we use a propensity score matching approach. Finally, we employ the sudden death of CEOs (Chief Executive Officers) as an exogenous shock to firms’ management, given their pivotal role in initiating and implementing corporate policies. A sudden death is expected to have a significant impact on managerial efficiency as it affects the ability to transform corporate resources into revenue. To address this causality issue, we run a difference-in-differences analysis. Overall, our base evidence remains robust across all these identification tests.

After establishing the relationship between managerial ability and audit outcomes, we perform several cross-sectional tests to examine the moderating effects of corporate governance, information asymmetry, client–auditor distance, and the industry specialization of auditors. We posit that managerial ability acts as either a complement to or a substitute for effective governance monitoring, better information quality, closer geographic proximity between the client firm and auditor, and the auditor’s superior industry specialism, in moderating the impact of these factors on the relationship between managerial ability and audit outcomes. From the perspective of complementary relationships, high-ability managers may benefit from these factors; their combined effects further mitigate audit engagement risk and effort. Such complementary relationships can further strengthen the association between managerial ability and favorable audit outcomes.

With regard to substitution effects, high-ability managers can offset the need for robust governance, mitigate the negative effects of high information asymmetry, compensate for the adverse impacts of greater distance between the auditor and the client firm, and reduce any reliance on auditor industry specialization. This is because high-ability managers possess extensive knowledge, managerial skills and expertise, industry networks, and strong professional reputations. Supporting these substitution effects, we find that the association between high-ability managers and favorable audit outcomes is stronger when the client firm experiences weaker governance monitoring and higher information asymmetry, is located further from the auditor, and associates with nonspecialist auditors.

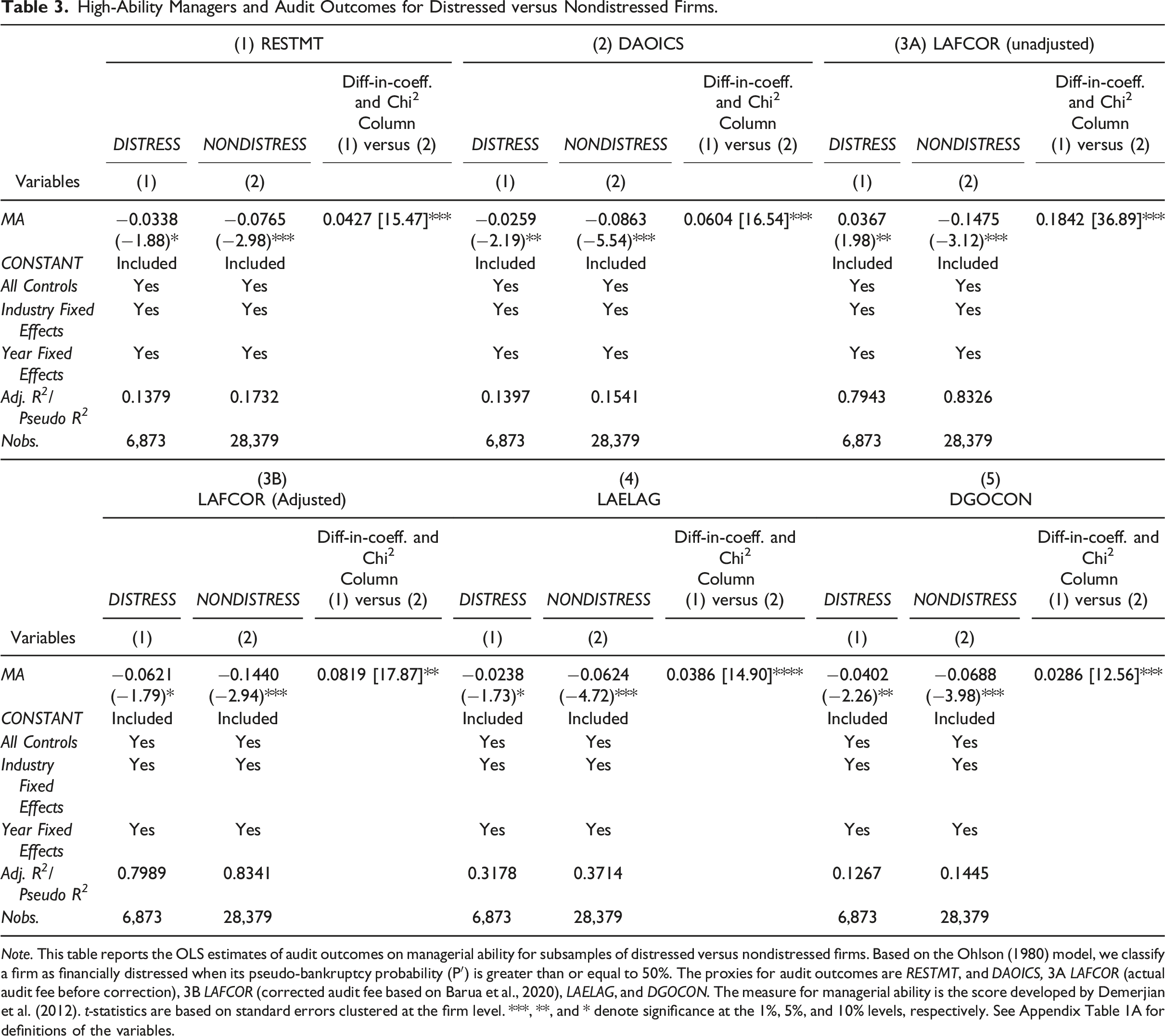

Our study makes significant contributions to the existing literature. First, our study contributes to the extant literature investigating the relationship between managerial ability and audit fees (Gul et al., 2018; Krishnan & Wang, 2015) and between managerial ability and audit report lag (Abernathy et al., 2018). From an audit fee perspective, Krishnan and Wang (2015) show a negative association between managerial ability and audit fees in general settings, whereas Gul et al. (2018) find a positive association in financially distressed firms. Our study supplements both studies by investigating the relationship in both general and financially distressed firms. Our results confirm a negative relationship between managerial ability and audit fees in general; however, this relationship becomes positive for highly distressed firms, consistent with Gul et al. (2018). Moreover, unlike other studies, we use a more accurate estimate of audit fees to mitigate the risk of mismeasurement. For example, prior empirical research (e.g., Lim & Monroe, 2022) tends to rely on the fees paid to the auditors as a proxy for audit fees, ignoring the audit fees of the successor and predecessor in years of auditor rotation. Audit fees tend to be significantly discounted in the auditor rotation year (Hay et al., 2006). This bias raises questions about the validity of earlier empirical works (Barua et al., 2020). Accordingly, we argue that correcting audit fees during the year of auditor rotation is critical, particularly if the relationship between managerial ability and audit fees is positive for distressed firms. However, after the correction, this relationship should shift to a negative association for distressed firms. Our empirical analysis indeed provides such evidence and demonstrates the significance of correcting audit fees. 3 Hence, our study provides robust evidence to reconcile the inconclusive findings of past studies.

In the context of audit report lags, our study adds a new dimension to Abernathy et al. (2018), by showing the distinct impact of managerial ability on highly distressed versus nondistressed firms. While Abernathy et al. find that higher managerial ability is associated with shorter audit report lag in general settings, our results confirm that this relationship is mainly prevalent for financially nondistressed firms. 4 Moreover, unlike this study, we employ a number of robustness tests that address endogeneity concerns related to managerial ability and audit report lag. Overall, our research offers new insights into policy and practice in this domain, emphasizing its originality and contribution to the existing body of knowledge.

Second, we add to the literature on the determinants of audit outcomes. As in prior research, audit outcomes are associated with accounting comparability (Zhang, 2018), financial statement footnote readability (Abernathy et al., 2019), accruals quality (Cho et al., 2017), auditor connectedness (Guan et al., 2016), and firm culture (Andiola et al., 2020). However, these studies have not explored the influence of managerial ability on three specific audit outcomes: the possibility of financial restatements, auditor assessment of internal controls, and the issuance of a going-concern opinion. Yet, we argue that audit outcomes, such as financial restatements, audit opinions of internal controls, and going-concern opinions, significantly impact regulators, corporate management, and other stakeholders (e.g., market participants and users of financial statements). For instance, the independence of auditor judgment assures the credibility of accounting information, effectively enabling capital market operations (Hanlon et al., 2022). Moreover, users of financial statements must rely solely on audit opinions (Herrbach, 2001), as they cannot access client firms’ accounting systems directly. Since the practical implications of these audit outcomes are crucial, we seek to add a valuable new dimension to this limited body of extant literature, by providing a comprehensive understanding of the distinct impact of managerial ability on various largely under-explored audit outcomes, such as financial restatements, going-concern opinions, and opinions on the strength of internal controls.

Third, in contrast to prior research, we provide new evidence on the moderating roles of corporate governance, information asymmetry, client–auditor distance, and the auditor’s industry specialism on the nexus between managerial ability and audit outcomes. We demonstrate that the relationship between managerial ability and audit outcomes is more pronounced for client firms that exhibit weak governance oversight, deal with severe information asymmetry, are located far from auditors, and lack industry-specific auditor expertise, supporting the case for the substitution effects of managerial ability. Hence, our study contributes to the body of literature (e.g., Armstrong et al., 2010; Baik et al., 2018; Frino et al., 2023; Lim & Monroe, 2022) on these four specific factors that are considered to be critical for ultimate auditor judgments and audit outcomes.

Finally, our analysis adds to the literature on factors that influence the likelihood of a lawsuit. According to prior research, such a likelihood is substantially affected by disclosure, social capital, and political corruption (Jha & Chen, 2015; Jha et al., 2021). Extending this stream of research, our distinct evidence demonstrates a lower litigation risk for firms managed by more able managers. Clearly, a firm’s managerial ability influences not only audit outcomes but associated risk as well.

We organize the remainder of our paper as follows. In section 2, we discuss the relevant literature and develop the hypotheses. Then, we present the sample and data, variables, and descriptive statistics in section 3. Subsequently, we provide the baseline evidence along with robustness and endogeneity tests in section 4. Finally, in sections 5 and 6, we highlight cross-sectional and additional analyses before concluding the paper in section 7.

Theoretical Literature and Hypotheses Development

There seems to be a noticeable shift in the theoretical framework used in contemporary accounting and auditing literature recently, moving from the neoclassical economic assumptions of management homogeneity toward upper echelons theory, which focuses on the idiosyncrasies and individual attributes in senior management (Bertrand & Schoar, 2003; Wells, 2020). This shift has largely been driven by the seminal study of Bertrand and Schoar (2003), which outlines the influence of “managerial style” on firms’ policies. The neoclassical view suggests that senior managers, such as CFOs (Chief Financial Officers), tend toward homogeneous decision-making driven by rational choices and that their individual style should not influence a firm’s accounting choices. In contrast, upper echelons theory recognizes how managerial idiosyncrasies affect managerial judgment and decision-making in business conduct in general and accounting practices in particular (Bertrand & Schoar, 2003). Following this theory, DeJong and Ling (2013) find that managerial style has a significant influence on accounting choices and financial reporting quality. Given this backdrop, as shown in Figure 1, we argue that high managerial ability could affect the quality of the client firm’s information environment and auditors’ assessment of client risk, which in turn could influence audit outcomes. We then clarify how various indicators in the information environment and the client risk perceived by auditors can mediate the association between managerial ability and audit outcomes. Conceptual framework: Managerial ability and audit outcomes. Source: Developed by authors based on a review of related literature and anonymous review comments.

Managerial Ability, Information Environment, Client Risk Assessment, and Audit Outcomes

A growing body of literature explains how managerial idiosyncrasies can influence the quality of the information environment by achieving higher-quality earnings and improved financial reporting quality, thereby affecting audit outcomes. Managerial idiosyncrasies and styles are important determinants of specific accounting choices, and they influence the usefulness of accounting information in decision-making (Wells, 2020). Demerjian et al. (2013) observe that superior managers possess greater knowledge of their business, client base, and macroeconomic conditions. Therefore, they make better judgments and more accurate estimates of accruals (such as bad debt estimates) and future cash flows, leading to higher-quality earnings.

Empirically, prior studies document that managerial ability is positively associated with the quality of earnings forecasts and accrual estimations (Baik et al., 2011; Demerjian et al., 2013), financial reporting quality (García-Meca & García-Sánchez, 2018), and the quality of a firm’s information environment (Baik et al., 2018; Wells, 2020). Doukas and Zhang (2020) argue that high-ability managers use discretionary accruals or earnings smoothing to provide more predictable cash flow and earnings, thereby reducing information asymmetries. Similarly, Abernathy et al. (2018) argue that high-ability managers, having more accurate judgments and estimates, can facilitate financial reporting and audit processes effectively and efficiently, reducing audit risk. Accordingly, they find that managerial ability reduces the earnings announcement lag and audit report lag. Overall, high-ability managers improve a firm’s information environment.

The positive influence of managerial ability on the quality of a client firm’s information environment may influence the auditor’s client risk assessment by positively shaping the credibility of the source of information and evidence. As auditors need to rely on management to gather extensive evidence during the audit process, it is critical for them to evaluate the credibility of the client-supplied sources (Kizirian et al., 2005). Jha and Chen (2015) argue that if auditors have high confidence in management, they tend to carry out fewer substantive procedures in the audit planning process, leading to less audit engagement. Dikolli et al. (2020) also assert that CEOs’ behavioral integrity enhances trust and credibility in the audit planning process, reducing audit engagement risk and audit fees. In the same vein, Jha and Chen (2015) concur that clients’ social capital or trustworthiness significantly influences the audit planning process, with a lower level of trust causing a longer audit report lag and higher audit fees.

Along with a creditable information environment, an auditor’s assessment of the quality of their client firm’s internal controls is a critical consideration in the audit planning process, as the auditor might perceive the need to exert more audit effort in a weaker internal control environment, giving rise to greater audit engagement risk (Balachandran et al., 2021). Likewise, Causholli et al. (2011) concur that control risk significantly determines audit effort, including the quality of a client’s control over financial reporting and an auditor’s stated reliance on such controls. In the context of our study, Kizirian et al. (2005) suggest that the “tone at the top” is an essential determinant of the auditor’s assessment of a client firm’s risk structure, as it provides a foundation for the client’s internal control. Judd et al. (2017) find that firms with narcissistic CEOs tend to exhibit higher internal control weaknesses, suggesting that auditors might need to perform additional procedures to assess elevated inherent risks when a firm has a narcissistic CEO. Thus, we argue that managerial competence can influence the internal control of client firms.

Finally, a few related studies explain how managerial ability can improve financial performance, reduce financial distress risk, and thus reduce audit engagement risk. For example, Shang (2021) refers to the managerial talent hypothesis wherein a more able management team evaluates the firm’s investment and growth opportunities more accurately and undertakes value-increasing projects, which boosts firm value and decreases liquidity risk and credit risk. In the same light, Huang and Sun (2017) argue that high-ability managers tend to manage firms’ resources more efficiently, leading to superior performance. Similarly, Krishnan and Wang (2015) show that greater managerial ability improves current and future firm performance and reduces a firm’s financial distress risks, eventually mitigating audit engagement risk. Likewise, Johnstone (2000) demonstrates a positive link between a client firm’s business risk and both audit risk and audit fees. Taken together, we can expect that managers with greater ability are more likely to be associated with favorable audit outcomes for their firms in terms of fewer financial restatements, a lower likelihood of adverse opinions on internal controls, lower audit fees, less audit effort, and a lower likelihood of going-concern opinions.

Nevertheless, highly capable managers may exhibit managerial entrenchment due to their superior skills and significant influence over decision-making processes and resource allocation (Demerjian et al., 2020). This exacerbates the risk of opportunistic behavior and enables managers to exploit their positions by manipulating corporate governance structures or bypassing oversight mechanisms. This behavior can take various forms, including favoring projects for personal reputation (or financial incentive), disregarding shareholder interests, and engaging in transactions that benefit related parties. Moreover, high-ability managers have greater opportunities to expand enterprise “empires,” potentially misusing free cash flow through over-investment by indulging in over-optimistic estimations of project cash flows (Chen et al., 2021). Consequently, the opportunistic behavior of high-ability managers is extensively discussed in the governance literature.

Prior studies also suggest that high-ability managers might engage in more improper accounting and unethical business practices, such as manipulation in financial reporting. For example, Gul et al. (2003) observe that high-ability managers’ subjective judgments and estimates of discretionary accruals are susceptible to manipulation, which is linked to a heightened assessment of inherent risk, leading to increased audit efforts and higher fees. Koester et al. (2017) report that high-ability managers carry out a higher degree of corporate tax avoidance to minimize costs and improve firm performance, tax avoidance being considered an unethical business practice. In sum, highly capable managers may indeed acquire a level of power that spurs them to conceal critical information and entertain unethical business practices, which will negatively affect the auditor’s client risk assessment and audit outcomes.

Considering these conflicting views around the relationship between managerial ability and audit outcomes, we draw on a balanced perspective that recognizes the dual impact of high-ability managers on audit outcomes. We initially highlight that a high-ability managerial team is more likely to enhance the quality of a firm’s information environment and shape the auditor’s client risk assessment through the higher perceived credibility derived from client-supplied evidence, stronger internal controls, and reduced financial distress risks. Specifically, in the presence of a high-ability managerial team in the client firm, auditors are more likely to assess the quality of the firm’s information environment and internal controls with less effort, leading to lower perceived audit engagement risk and favorable audit outcomes. However, we further acknowledge that highly capable managers who have gained significant power and become entrenched can undermine organizational integrity and information transparency, potentially causing unfavorable audit outcomes for the client firm. In considering the tension between the two propositions, we contend that transitioning from virtuous managerial capability toward opportunism features a complex interplay between managerial competence and ethical conduct. This interplay itself might lead to either favorable or unfavorable audit outcomes for the client firm. By offering a balanced perspective, we aim to comprehensively understand this complex relationship. Accordingly, we develop the following nondirectional hypothesis:

Moderation Effects on the Relationship Between Managerial Ability and Audit Outcomes

In this section, we elucidate how governance monitoring, information asymmetry, client–auditor distance, and auditor industry specialism moderate the associations between managerial ability and audit outcomes.

The Moderating Effects of Corporate Governance

The influence of the interaction between managerial ability and corporate governance on audit outcomes is a complex landscape that can be viewed through a “complementary” or “substitution” lens. The complementary hypothesis suggests that effective corporate governance in client firms establishes accountability, improves transparency, and prevents managers from engaging in unethical practices by increasing checks and balances. For example, McCahery et al. (2016) argue that institutional investors, their presence being an indicator of good governance, adopt various exit and voice strategies to improve governance monitoring and reduce managerial entrenchment in their portfolio companies. Stronger governance mechanisms are also likely to strengthen the internal control environment of the client firm (Chen et al., 2017) and reduce earnings manipulation risk (Bedard & Johnstone, 2004). Moreover, Chen et al. (2006) find that good governance, measured by a high proportion of nonexecutive directors and high board meeting frequency, diminishes the likelihood of firms engaging in fraud, while Pae and Choi (2011) show that firms with effective governance are more committed to business ethics. Finally, Armstrong et al. (2010) observe that stronger monitoring mechanisms reduce moral hazard problems. Considering such positive aspects of robust governance, García-Sánchez and García-Meca (2018) report that internal governance mechanisms, such as board effectiveness, reinforce the positive effect of managerial ability on investment efficiency, suggesting a complementary relationship between corporate governance and managerial ability.

The discussion above suggests that high-ability managers can foster greater transparency and reliability in firms with robust governance. This synergy between managerial ability and governance monitoring can meaningfully decrease audit engagement risk. Moreover, efficient governance mechanisms reduce the opportunistic behavior of high-ability managers, thereby improving the information environment. Thus, the complementary relationship between strong governance and high managerial ability may reduce a firm’s audit engagement risk, resulting in favorable audit outcomes.

In contrast, managerial ability can also act as a substitute for governance monitoring. The substitution hypothesis holds that weaker monitoring may increase agency conflicts and informational asymmetries between shareholders and managers due to moral hazard problems (Armstrong et al., 2010), causing a deterioration of a firm’s information environment. In this context, auditors may rely more on the credentials of high-ability managers to determine the audit engagement risk, as the latter can independently maintain high information quality and operational efficiency. This suggests that capable managers might act as a substitute for inadequate governance monitoring by reducing engagement risk, thereby fostering favorable audit outcomes.

Considering the two opposing lines of argument, we posit that the effect of the interaction between managerial ability and governance on audit outcomes is explained by either a complementary or substitution hypothesis. Accordingly, we develop the following incompatible hypotheses:

The Role of Information Asymmetry

The relationship between managerial ability and audit outcomes might be influenced by information asymmetry, a condition where external stakeholders, including auditors, encounter difficulties in accurately evaluating financial data. As discussed earlier, the quality of a firm’s information environment plays a significant role in shaping a firm’s audit outcome. An environment with high information asymmetry increases audit engagement risk, as the auditor needs to spend more time and effort collecting and processing necessary information during the audit (Balachandran et al., 2021; Frino et al., 2023). This infers that less transparent firms have a greater propensity to conceal information from auditors and the public, making it difficult for auditors to provide an accurate representation of them (Frino et al., 2023). Consequently, auditors exercise greater “professional skepticism” and prudence in assessing poor-quality financial reporting, so they have to exert greater audit effort and, hence, charge an audit premium (Jha & Chen, 2015). Likewise, Balachandran et al. (2021) observe that auditors are likely to respond to a poor-quality client–firm information environment by recommending financial restatements, issuing a going-concern opinion, or forming an adverse opinion on internal controls. Call et al. (2017) report an inverse association between the quality of the information environment and financial restatements.

In the context of low information asymmetry, we argue that high-ability managers are in an advantageous position to play a pivotal role in shaping the quality and transparency of financial reporting by facilitating clearer and more trustworthy financial disclosure (Baik et al., 2018; García-Meca & García-Sánchez, 2018; Wells, 2020). High managerial ability and low information asymmetry could work together to reduce the perceived engagement risk for auditors. Thus, low information asymmetry is likely to reinforce the relationship between managerial ability and audit outcomes (Abernathy et al., 2018; Doukas & Zhang, 2020).

However, in environments with high information asymmetry, auditors might rely on high-ability managers as they have greater professional integrity in the industry. Auditors may place higher trust in these managers for credible sources of client-supplied evidence, believing that their professional reputation will compensate for any lack of information. Moreover, high-ability managers are presumed to be more effective in implementing risk mitigation strategies (Bonsall et al., 2017). Such perception may lead auditors to lower their risk assessments, affecting audit outcomes favorably. Nevertheless, one may argue that opportunistic high-ability managers might exploit this poor information environment to conceal and manipulate information. As a result, the positive effect of managerial ability on audit outcomes could be diminished.

Taken together, the above arguments suggest that information asymmetry plays a crucial role in the impact of managerial ability on audit outcomes. Accordingly, we also develop the following incompatible hypotheses:

The Role of the Distance Between Auditor and Client Firm

Auditors’ geographic proximity to their client firms might reinforce the relationship between managerial ability and audit outcomes. On the one hand, auditors closer to their client firms are likely to have information and monitoring advantages. Choi et al. (2012) claim that local auditors have better access to client-specific knowledge than their nonlocal peers. Moreover, local auditors can more frequently interact with their client firms and learn of client-specific incentives, their modus operandi, and negative reporting from local media, all of which enhance auditors’ capacity to efficiently monitor the client (Kang & Kim, 2008). The comparative convenience of greater knowledge and monitoring efficiency enables local auditors to mitigate aggressive and biased reporting practices (Krishnan, 2003). Several studies provide empirical evidence to support this argument. For example, Choi et al. (2012) find that the informational advantage of auditors being local effectively empowers them to constrain management from biased earnings reporting, leading to higher-quality audits. Similarly, Dong and Robinson (2018) demonstrate that audit reports are timelier for geographically proximate auditor clients.

The information and monitoring advantage of auditor proximity is likely to reinforce the positive effect of managerial ability on audit outcomes. Under this assumption, high managerial ability and close auditor–client proximity could work together to reduce engagement risk, resulting in favorable audit outcomes. On the other hand, a higher information asymmetry associated with a greater geographic distance might compel auditors to rely more on high-ability managers as a trustworthy source of client-supplied evidence. Therefore, we contend that managerial ability is likely to have a greater impact on audit outcomes even when the client firm is located further from the audit firm as high managerial ability can address the negative effects of greater distance between the auditor and the client firm on audit outcomes. Consequently, high-ability managers could be substitutes for mitigating the adverse effect of greater auditor–client distance on the association between managerial ability and audit outcomes. Considering these contradictory arguments, we develop the following incompatible subhypotheses:

The Role of Auditors’ Industry Specialism

Auditors with specialist expertise in a particular industry are likely to positively impact financial reporting and audit quality as they possess superior industry-specific knowledge and understanding. The growing empirical literature provides evidence of this positive relationship. For example, Dunn and Mayhew (2004) report that clients of industry-specialist audit firms have greater information disclosure quality than clients of nonspecialist audit firms. Balsam et al. (2003) also find that clients of industry-specialist auditors have a lower absolute level of discretionary accruals and earnings response than nonspecialist auditors. Likewise, Fleming et al. (2014) find that auditor industry specialism helps to reduce audit fees during the first year of Sarbanes–Oxley Act (SOX) compliance. The preceding arguments and evidence suggest a positive association between specialist auditors and favorable audit outcomes, implying that high-ability managers may benefit from specialized auditors’ deeper insights and more rigorous assessments. Therefore, auditors’ industry specialization might play a complementary role to managerial ability, in leading to optimal client firm audit outcomes.

However, we argue that a substitutive relationship is also possible as high managerial ability might diminish the need for auditor industry specialization in achieving favorable audit outcomes for the client firm. As presented earlier, high-capability managers have superior knowledge and skills to effectively monitor a firm’s financial reporting processes, implement robust internal controls, and assure an accurate and transparent information environment. These capabilities could compensate for the absence of auditor specialism. Consistent with this argument, we contend that when auditors are not experts in their client firms’ industries, they are likely to depend more on high-ability managers when undertaking client risk assessments. Considering these opposing lines of arguments, we test the following incompatible subhypotheses:

Research Method

Data and Sample

To compile a comprehensive sample from publicly listed US firms, we use data from various sources spanning the years 2000 to 2018, since 2000 is the first year when information on audit outcomes (such as financial restatement, internal controls, audit fees, restatement and going-concern opinions) emerges in the Audit Analytics database. We access Demerjian’s webpage, Compustat, Thomson Reuters Institutional Holdings (13F), Institutional Brokers’ Estimate System (I/B/E/S), and BoardEx to obtain measures of managerial ability, firm characteristics, institutional ownership, analyst coverage, and board independence. 5 To regress audit outcomes on managers’ ability and derive our final sample, we apply the following filters: (i) limiting sample years to firms with at least two consecutive years of data and excluding observations without the managerial ability score; (ii) removing observations from years where total assets are less than USD 1 million (Balachandran et al., 2021; Barua et al., 2020); (iii) dropping observations from regulated utility and financial industries (Xu et al., 2019) 6 ; and (iv) using a modified or corrected measure of audit fees of the successor and predecessor in the year of an auditor change (Barua et al., 2020). The final sample comprises 35,252 firm-year observations from 3987 nonfinancial firms over 19 years.

Measures of Managerial Ability and Audit Outcomes

The main explanatory variable is managerial ability (

The key dependent variable is audit outcomes (

Model Specification

To investigate the relationship between managerial ability and audit outcomes, we use the following specification in equation (1):

Consistent with earlier studies (Balachandran et al., 2021; Hay et al., 2006; Krishnan & Wang, 2015; Ma et al., 2021), we control for: firm size (

Descriptive Statistics and Correlation Matrix

Descriptive Statistics.

Table 2A in the appendix presents a matrix indicating correlations among measures of managerial ability, audit outcomes, and other variables. Our analysis shows a negative correlation between managers’ ability and the audit outcome measures, suggesting that firms led by high-ability managers are likely to benefit from auditing services. Further, the correlation coefficient among controls is less than 0.7 in absolute value, which mitigates concerns about multicollinearity. Theoretically, coefficients equal to or exceeding 0.7 in absolute value indicate multicollinearity issues (Liu et al., 2014). Given that our empirical settings adhere to this general rule, multicollinearity is unlikely to affect our analyses.

Empirical Results

Baseline Evidence

High-Ability Managers and Audit Outcomes: Base Evidence.

The coefficients of the controls are consistently significant across most audit outcomes. 11 It is evident that larger firms (Ali et al., 2022; Xu et al., 2019), those paying higher nonaudit fees (Ali et al., 2022), those experiencing income losses (Hope et al., 2017; Xu et al., 2019), those audited by Big Four firms (Hope et al., 2017), those with more complex operations such as multiple segments and foreign operations (Krishnan & Wang, 2015; Xu et al., 2019), those with a high market-to-book ratio (Ali et al., 2022), and those facing higher litigation risk (Xu et al., 2019) and inherent risk (Ali et al., 2022), experience unfavorable audit outcomes. These outcomes include more financial restatements, a higher likelihood of adverse opinions on internal controls, higher audit fees, longer audit report lags, and a higher likelihood of receiving going-concern opinions. However, firms with strong asset returns tend to experience fewer restatements, are less likely to receive adverse opinions on internal controls, and pay lower audit fees (Hope et al., 2017; Ma et al., 2021).

Overall, our evidence confirms and supports our baseline hypothesis (

High-Ability Managers and Audit Outcomes for Distressed versus Nondistressed Firms.

Robustness Test

To confirm the reliability and robustness of our baseline findings, we perform a change analysis on any change in the variables of managerial ability, audit outcomes, and all the controls. The changes are calculated by the variation in the respective variable from year t-1 to year t. Our un-tabulated results suggest that the coefficient of △

Endogeneity Tests

This sub-section addresses potential endogeneity issues surrounding the relationship between managerial ability and audit outcomes. We undertake several approaches, namely, firm-fixed effects (FFE), instrumental variables (IV), propensity score matching (PSM), and difference-in-differences (DiD), to ensure the robustness of our main findings against endogeneity concerns.

Firm-Fixed Effects

Unobserved firm-level time-invariant characteristics are likely to affect the robustness of our relationship between managers’ ability and audit outcomes. To mitigate this concern, we reestimate equation (1) employing the FFE regression model. Table 3A in the appendix presents the results. We find that firm-fixed effect results are qualitatively similar to the OLS regressions in Table 2 in terms of sign, magnitude, and significance. This validates our baseline results and confirms that the firm-specific omitted variables do not drive our findings. We further examine whether unobserved auditor-level characteristics lead to an under-specification bias. We alleviate this concern by conducting auditor effects and the city of the auditor fixed effect in our baseline regressions. Our results in Appendix Table 4A confirm that the relationship between managerial ability and audit outcomes remains robust even after considering auditor-level heterogeneity.

Instrumental Variable Approach

Our baseline results indicate that a high-ability manager is associated with favorable audit outcomes. However, one may argue that our results are driven not by managerial ability but by inherent heterogeneity in preferences. To mitigate this concern, we use an instrumental variable (IV) approach, using the technique developed by Lewbel (2012). This 2SLS technique utilizes heteroskedasticity in the data to create internal instruments for a 2SLS regression. Many prior studies (e.g., Chen et al., 2015; Hasan, 2020) have employed this approach in accounting and finance research due to the challenges in finding suitable exogenous instruments.

Endogeneity Tests: Instrumental Variable (IV) Approach.

Propensity Score Matching

Our baseline results could also be subject to other possible endogeneity concerns. For example, one may contend that firms with higher-ability managers and those with lower-ability managers are essentially distinct types of firms. In other words, firm-level attributes can significantly differ between firms with high-ability and low-ability managers. We employ propensity score matching to address the concern that the two groups are indistinguishable in their firm characteristics.

To execute the propensity score estimate, we divide our sample into subsamples of firms with high-ability and low-ability managers. Firms with high managerial ability (above the yearly two-digit SIC industry median) are our treatment firms, while firms with low managerial ability are our control firms. To ensure that the firm-year observations in both groups are identical regarding observable attributes, we compare the mean difference of each control variable used in the baseline regression between the treatment and control firm-year observations.

Endogeneity Tests: Propensity Score Matching (PSM) Analysis.

Difference-in-Differences: Sudden Deaths of CEOs

Our fourth approach to addressing endogeneity concerns is to examine changes in managerial ability when a firm experiences its CEO’s sudden death. Chang et al. (2010) suggest that the CEO is the major contributor to a firm’s decisions, skills, experience, and leadership qualities. Thus, unexpected CEO turnover due to premature death is likely to have a negative impact on a firm’s managerial ability. We contend that CEO sudden deaths are perfectly exogenous events as they are neither planned nor driven by poor managerial performance. Therefore, we examine the effects of managerial ability on audit outcomes following the sudden deaths of CEOs by using the difference-in-difference (DiD) framework.

If the relationship is causal, we will find that managerial ability is associated with unfavorable audit outcomes for the client firm due to a decline in managerial ability after the CEO’s death. To empirically test our assertion, we collect CEO turnover data from Gentry et al. (2021) and identify 19 incidents of CEO turnover due to death. Following Gormley et al. (2013), we construct our treatment and control group cohorts. We consider each CEO’s death year as a cohort and utilize 2 years before and after this exogenous event. In each cohort, we allocate firms to the treatment group if they experienced a sudden CEO death; otherwise, we allocate them to the control group if they did not experience such a shock.

To validate our assumptions about whether managerial ability decreases after a CEO’s sudden death, we plot the managerial ability of both treatment and control firms around the event. Figure 1A in the Appendix illustrates this comparison. We demonstrate that the managerial ability of the treatment firms declines following the sudden demise of a CEO, thereby validating the CEO’s sudden death as an exogenous shock for our DiD approach.

Endogeneity Tests: Difference-in-Difference (DiD) Approach.

We also examine the parallel trend assumption of a DiD estimation. We replace

Other Endogeneity Tests

In addition to the above, we use the yearly two-digit SIC industry median firm-level managerial ability as an instrument in the first-stage regression. We then reestimate equation (1) using the fitted values of managerial ability. The results reported in Appendix Table 5A show that our instrument is positively related to the endogenous variable (

Moderation Analyses

The Role of Corporate Governance

First, we investigate the moderating effect of corporate governance on the relationship between managerial ability and audit outcomes (

Moderating Effect of Governance Monitoring—Board Independence.

The Role of Information Asymmetry

Moderating Effect of Information Environment—Analyst Following.

Our second test examines how the probability of insider trading affects the relationship between managerial ability and audit outcomes. The variable for the probability of insider trading (

The Role of Distance Between Auditor and Client Firm

Moderating Effect of the Distance Between Audit Office and Client Firm.

The Role of Auditor Industry Specialism

Moderating Effect of Auditors’ Specialization.

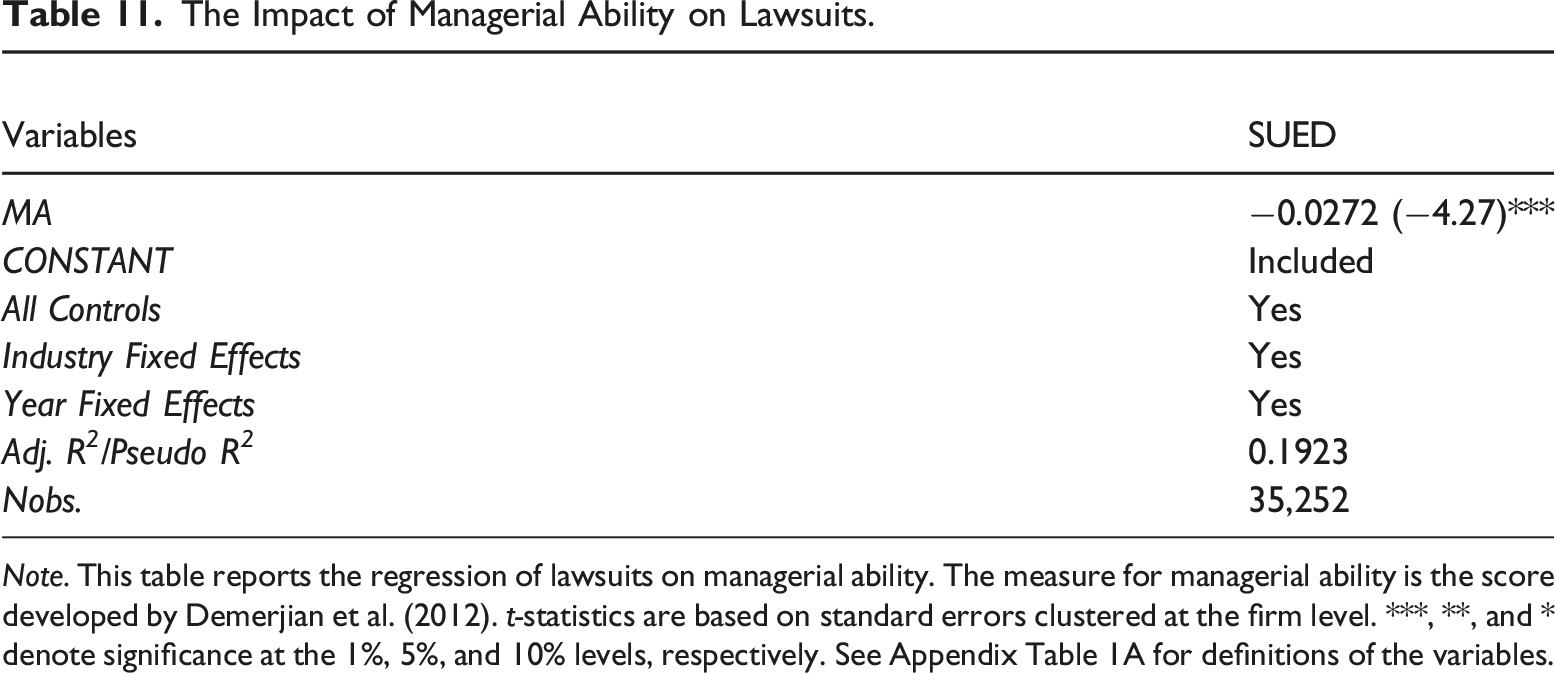

Additional Tests: Managerial Ability and Lawsuit

From our main analysis, we establish a significant association between managerial ability and audit outcomes. This section extends our analysis to estimate whether there is any impact of a high-ability manager on the likelihood of a lawsuit. Effective monitoring by a more able manager is likely to reduce information asymmetry, improve information disclosure, and result in fewer restatements. Therefore, we expect that greater managerial ability should diminish the risk of lawsuits against the firms. Following Jha and Chen (2015) and Jha et al. (2021), we create

The Impact of Managerial Ability on Lawsuits.

Conclusion

This study examines the role of managerial ability in shaping major audit outcomes, namely, financial restatements, opinions on internal controls, audit fees, audit effort, and the likelihood of receiving a going-concern opinion. Using a large sample of 35,252 firm-year observations from publicly listed US firms spanning 2000 to 2018, our analysis reveals negative relationships between managerial ability and audit outcomes. These indicate that client firms with high-ability managers exhibit fewer financial restatements, a lower probability of adverse opinions on internal controls, lower audit fees, reduced audit effort, and a lesser likelihood of receiving a going-concern opinion. These findings remain robust across alternative econometric specifications, including firm-fixed effects, an instrumental variables approach, propensity score matching, and difference-in-differences analysis using sudden CEO deaths as an exogenous shock. Our cross-sectional analyses further highlight that managerial ability exerts a stronger negative influence on audit outcomes under conditions of weaker governance oversight, poor information environments, greater auditor–client distance, and nonspecialist auditors, supporting the case for the substitution effects of managerial ability. Finally, our additional analysis shows that firms with greater management ability face a reduced likelihood of lawsuits.

The implications of our findings extend to various stakeholders, including firms, auditors, and policymakers.

Supplemental Material

Supplemental Material - Managerial Ability and Audit Outcomes

Supplemental Material for Managerial Ability and Audit Outcomes by Faizul Haque, Prem Puwanenthiren, Md Samsul Alam, and Sivathaasan Nadarajah in Journal of Accounting, Auditing & Finance

Footnotes

Acknowledgements

We are thankful to the Editor, Associate Editor, and the anonymous Reviewer for their invaluable comments and feedback, which have greatly enhanced the quality of our manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.