Abstract

Microfinance was initiated with the objective to alleviate poverty by income-generating small loans to the unbanked poor. The success was recognized by the world, as evidenced with the United Nations (UN) declaring the year 2005 as the ‘International Year of Microcredit’. In the very next year, 2006, the Nobel Peace Prize was awarded to the

The Indian microfinance sector, one of the leading markets in the world, has also experienced fundamental changes in the structure of ownership, control, and management of modern-day MFIs, as well as in changing stakeholder commitments (Nair, 2010). The sector has expanded enormously over the last 2 decades. However, the sector also witnessed its greatest ever shock, the Andhra Pradesh crisis, during 2005–2017. The crisis brought numerous regulations in response, which altered the dynamics of the Indian microfinance market. It is crucial to analyze the effect of these developments in the market structure on the competitiveness of the sector. Table 1 depicts the Herfindahl–Hirschman Index (HHI) and the

REVIEW OF LITERATURE

Market Concentration and Competition

The established opinions find the concentration of the market detrimental to competition. According to the structure–conduct–performance (SCP) hypothesis (Bain, 1951, 1956), a rise in concentration hurts the competition level in a market and provides market power to the individual firms to earn extra profit. A competing ideology, the efficient structure hypothesis (Demsetz, 1973) offers an alternative explanation for this positive relationship between concentration and profitability. It argues that efficient banks gain greater profitability and market share. As a result, the market becomes more concentrated. Another hypothesis, relative market power hypothesis (Shepherd, 1982, 1986) proposes that the performance of a firm is explained by efficiency as well as by its market share. The quiet life hypothesis,

1

According to quiet life hypothesis, power to charge price above marginal costs does not motivate managers to work efficiently. The market power provides shield to incompetent managers.

However, this view is criticized on the ground that higher concentration does not always indicate the absence of competition (Bikker & Haaf, 2002b). Recent research has contended that the relationship between concentration and competition is not as straightforward as assumed by the structural approaches. Consolidation can be a response to high competition (Berger, Bonime, & Hancock, 2000; Bikker & Spierdijk, 2009). Even there can be no relationship between market power and concentration (Fernandez de Guevara, Maudos, & Perez, 2005; Weill, 2013). The alternate views, termed as new empirical industrial organization (NEIO) approaches stress on the study of competitive conduct of firms to test competition and market power without paying attention to the structure of the market (Bikker & Haaf, 2002a). However, the findings of empirical research on banking sector lack consensus on the cause and effect relationship between market concentration and the level of competition.

Competition and Microfinance

Theoretical and empirical studies find an association between competition and financial stability and conduct of prudential policies with respect to banks (Bikker, Spierdijk, & Finnie, 2007). The competition–stability hypothesis postulates that competition improves financial depth in the banking sector (Dick & Lehnert, 2010; Rice & Strahan, 2010). It brings stability (Acs & Audretsch, 1988; Boyd & De Nicolo, 2005; Mitton, 2008) and efficiency (Bertrand, Schoar, & Thesmar, 2007) in the institution.

On the microfinance sector, the outcome of the competition is not as simple and straightforward as it is in the banking sector. Microfinance institutions differ from mainstream banks on two main issues. First, their primary objective goes beyond earning profits and, second, their business involves higher risk. This way they pursue the double bottom line; the social and the financial obligations (Mersland & Strom, 2010). Their social objective goes far beyond providing services in a business-like way.

2

For many of them, providing financial services has been just a means to achieve their social objectives. Many NGOs in African countries have registered themselves as ‘profit making entity’ in order to provide microfinance services to the poor (Navin, 2015).

Before the commercialization of the microfinance business, most of the MFIs were operating as monopolists (CGAP, 2001; McIntosh & Wydick, 2005). Under monopoly, an exploitative lender can systematically squeeze the borrowers by charging a high rate of interest

3

High interest rates do not always imply monopoly and inefficiency. They may reflect the high costs of doing business or high opportunity costs. Often used to refer joint liability lending where borrowers have to form small groups and require to guarantee each other’s (of her group) loan repayments. This way their incentives align with that of the lender.

The structure of the modern-day microfinance sector has changed significantly. Commercial MFIs are operating in the business and, the focus of the microfinance business has shifted from socially oriented ‘poverty lending’ approach to an institution-oriented ‘financial systems’ approach (Hulme & Arun, 2009). These developments have made the market highly competitive. A highly competitive market with no entry barriers confirms that MFIs break even and provide credit opportunity to all borrowers. This restricts the ability of MFIs to demand higher interest charge per units. However, due to information asymmetry among the MFIs about the loan default cases, borrowers can go for multiple borrowings with no intention to pay back. This surely improves the welfare of some borrowers; however, lowers the welfare of the poor and honest clients. Backed by theoretical models, Hoff and Stiglitz (1997), Kranton and Swamy (1999), and Van Tassel (2002) argue that intense competition adversely affects the performance of MFIs. It increases the chances of enforcement externality and will compel MFIs to increase interest rates (Guha & Roy Chowdhury, 2013). Lahkar and Pingali (2016) put forward a theoretical model to show that even in case of an increase in the interest rate and loan default due to rise in competition, borrower welfare may still improve with the expansion of microfinance industry.

Recent empirical investigations on competitive conditions in the microfinance sector have focussed on issues of outreach, adverse selection, multiple borrowings, and loan default. In their study on the two leading MFIs of Bolivia, Navajas, Conning, and Gonzalez-Vega (2003) find that though the increase in competition brings innovation which helps MFIs to expand their outreach, it decreases the MFIs’ ability to cross-subsidize smaller loans to poorer borrowers. Vogelgesang (2003) finds that a rise in the competition level adversely affects MFIs’ financial performance. In such market conditions, MFIs compromise with their social objectives (Olivares-Palanco, 2005) as it limits their ability to cross-subsidize their loans to the poorer clients (McIntosh & Wydick, 2005;). Cull, Demirguc-Kunt, and Morduch (2009b) find that tough competition from mainstream banks often reduces MFI’s breadth of outreach. Rosenberg (2010), Schicks and Rosenberg (2011), and Assefa, Hermes, and Meesters (2013) find a rise in competition level adversely affects the outreach, efficiency, and loan repayment of MFIs. De Quidt et al. (2018) study the effects of market power on the microfinance sector through estimating borrowers’ welfare under different market conditions. They find a trade-off, the enforcement externality under perfect competition with high profit-making under monopoly. In his study on the microfinance sector of Bangladesh, Mia (2018) finds that the sector is moving towards less concentration and the competition level is rising. Kar (2016) applies the Boone indicator in a cross-country study and finds a rise in competition level in the Indian microfinance sector during 2003–2010.

So far, no literature has focussed explicitly on the market structure of the Indian microfinance sector. Most of the studies on measuring the competition level of the microfinance sector are cross-country analysis. However, they do not provide a detailed discussion of the market structure of the Indian microfinance sector. Although India is one of the fastest-growing economies in the world, achieving inclusive growth remains one of the top priorities for the country. Access to financial services plays an important role in ensuring inclusive growth. In India, a significant number of people are still financially excluded. A study on the Indian microfinance sector is crucial to understand the present scenario of the sector. It will help the policymakers to design appropriate policies for financial inclusion. The current study contributes to the existing literature in numerous ways. It analyzes the market structure and measures the competition level of the Indian microfinance sector. Furthermore, it attempts to find the causes behind the change in the market structure of the sector. The study also analyzes the performance of leading MFIs having the market power in order to comment on their conduct.

RESEARCH METHODOLOGY

Panzar and Rosse (1987) formulated a statistic to measure the competitive conditions in a contestable market. The model explains ‘competition’ as a definite competitive behaviour and attempts to measure its intensity as an average overall banking product (Bikker & Spierdijk, 2009). It measures the market power by the amount to which a change in the factor input prices gets reflected in the equilibrium bank-specific revenues (Goddard & Wilson, Competition in banking: A disequilibrium approach, 2009). The main advantage of the methodology lies in its efficiency in capturing the outcome of a relative change in the marginal, total, or average cost curve even in the absence of cost data (Panzar & Rosse, 1987). While applying the Panzar and Rosee (PR) method on MFI data, MFIs are deemed as profit-maximizing entities providing homogeneous single product and, their cost structure is homogenous (Bandt & Davis, 2000; Bikker, 2004; Shaffer, 2004).

Theoretical Framework of Panzar–Rosse (PR) Model

The empirical test of the PR measure is grounded on the equilibrium model that sets the equilibrium output by maximizing profits. Profit maximizes where

Where

The second rule infers that the industry must hold the zero-profit level constraint. Furthermore, it is assumed that the cost structure of all MFIs is homogenous (Bandt & Davis, 2000; Bikker, 2004; Shaffer, 2004).

The functional form of the profit equation is:

Where

The model measures the degree of competitiveness with the help of an index known as ‘PRH’ or ‘H-statistics’. The H statistic is the sum total of elasticities of the revenue

The H-statistic value ranges between − ∞ < H ≤ 1, where H = 0 implies a full monopoly market condition and H = 1 refers to perfect competition. The value of the H-statistic between 0 and 1 reflects a variety of scenarios of monopolistic competition, having different degrees of competition intensity (Goddard & Wilson, 2009).

Despite so many merits, the PR measure is not without limitations. The H-statistic does not vary over time, making it less relevant to investigate the evolution of competition (Koetter, Kolari, & Spierdijk, 2012). Furthermore, it mensurates competition at the industry level. It is not possible to measure competition at the firm level using this measure.

Model Specification and Estimation

Applying the logic of the PR model, equilibrium conditions can be featured as a steady state reflecting adjustment to shocks (Buchs & Mathisen, 2005). The estimate of H-statistic is attained by altering the PR model in the following econometric specification:

where,

The main assumption of the method is that the market at each point of time is in the long-run equilibrium state. The equilibrium condition is tested by estimating the following equation with return on assets (ROA)

5

Shaffer (1982) suggested the use return-on-assets (ROA) as dependent variable to calculate long-run E-statistic.

Where,

ROA

PAR30 = Portfolio at risk. It is the proportion of MFI’s loan portfolio unpaid for more than 30 days. It is used as a measure risk scenario of an MFI.

TA = Total assets.

CA = Equity-to-assets ratio.

GDP = GDP growth rate.

The equilibrium E-statistic is the aggregate of the elasticities of factor input prices. It is calculated as follows:

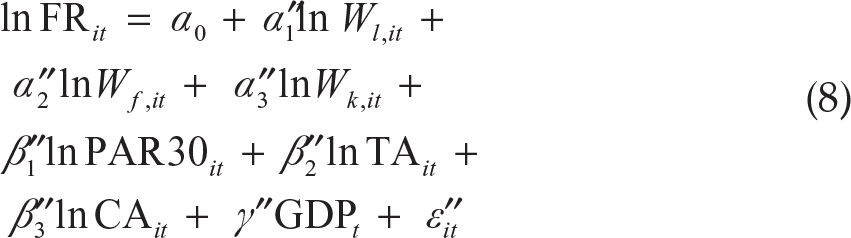

The H-statistic is estimated by the transformation of the PR revenue test into the following econometric equation having financial revenue (FR)

6

Due to inconsistency in ‘Other Income’ data of MFIs, the current study decided to measure the level of competition among MFI only at its main activity using the financial revenue FR as a dependent variable. Financial revenue comprises all the income generated from MFI’s core activity of providing financial services.

The dynamic version of Equation (8) will take the following form:

The PRH statistic is the sum total of the coefficients of factor inputs of Equation 9,

The aforementioned equations are estimated to measure the level of competition in the Indian microfinance market. Microfinance institution specific effects are removed by taking the difference of the equation. To remove the endogeneity problem due to the use of lagged dependent variable as an independent variable, the difference generalized methods of moments (GMM) estimator offered by Arellano and Bond (1991) is applied as suggested by Goddard and Wilson (2009) and Olivero and Jeon (2011). In difference GMM, estimators are obtained using the moment conditions generated by the lag of dependent variable with the difference disturbance term (Δv

Misspecification of PRH-Statistic

The current study deals with the following two misspecifications of the PRH statistic. First, PRH needs the state of market equilibrium for reliable estimation of competition levels reflected by H-statistic. However, in practice, often the market is not in an equilibrium state and the speed of adjustment towards equilibrium is not instantaneous but partial (Goddard & Wilson, 2009). The partial adjustment necessitates constructing a dynamic revenue equation. Use of the dynamic equation model has also been advocated from the perspective of time-series (Goddard & Wilson, 2009). It is formulated that if revenue of a firm is actually dependent upon its previous year revenue, the application of static estimation would contain a pattern of autocorrelation in the disturbance terms. Furthermore, the dynamic model estimation is also required to find the perseverance of profit (Sinha & Sharma, 2018) as it is not always the case that the observed profit is an equilibrium value (Berger et al., 2000; Goddard, Molyneux, & Wilson, 2004a, b).

Bikker, Spierdijk, and Finnie (2006) pointed out another misspecification of the method. According to him, the scaled form of income as the dependent variable in the revenue equation converts the revenue equation into a price equation. This alteration has a strong bias of H-statistic near 1. Therefore, the current study uses the unscaled value of FR in the revenue equation as a dependent variable.

DATA

The current study used MFI-level data of 127 MFIs of different legal statuses for a period of 12 years from 2005 to 2017. The main source of data is the MIX Market database.

7

Descriptive Statistics of Independent Variables

The cross-correlations among all the independent variables are checked. It is found that all the variables have correlation well below 0.80 (or 80%). The Unit root test is conducted to check for the stationarity of the sample data. The final estimation model contains the log value of all the variables except the GDP growth rate.

EMPIRICAL RESULTS

A static version of the PR method is applicable only under the equilibrium market conditions, therefore a test for equilibrium conditions is conducted. The Wald test rejects the null hypothesis for the presence of equilibrium indicating the presence of disequilibrium in the sector during 2005–2017. Therefore, a dynamic revenue equation is applied for the estimation of H-statistic.

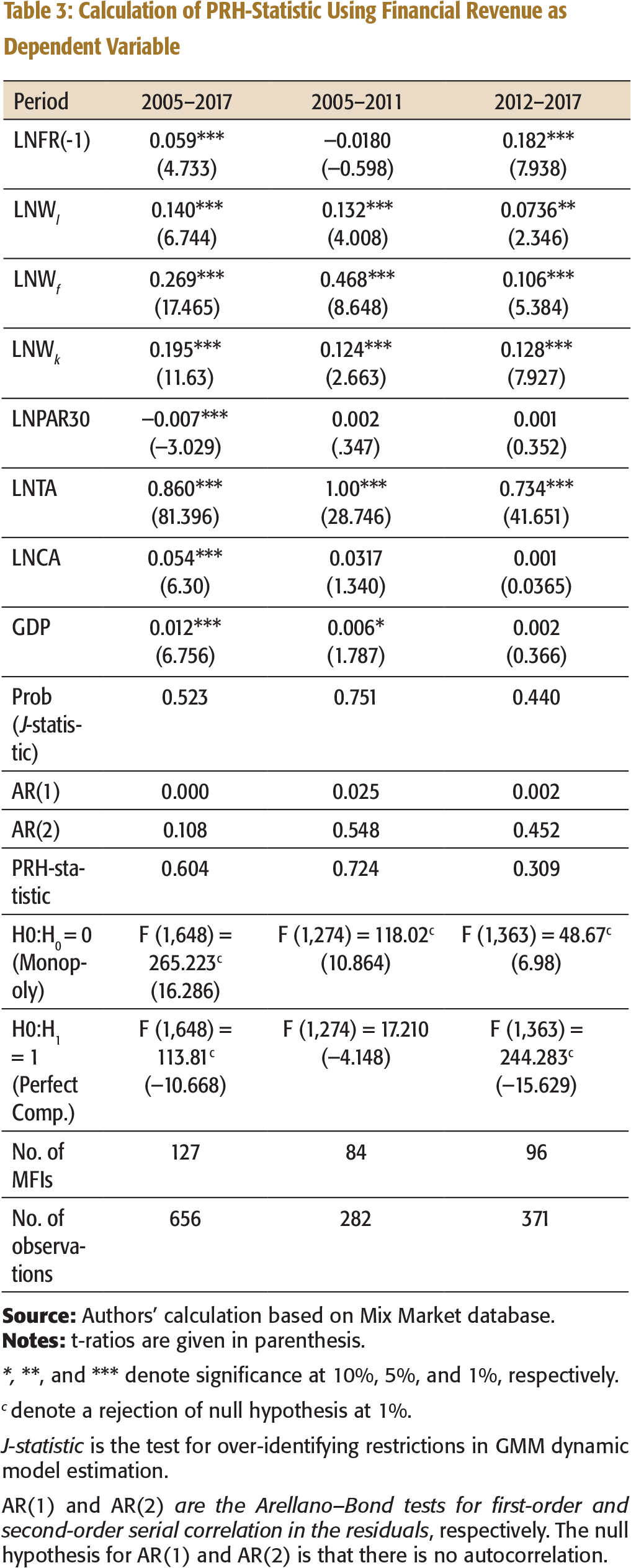

Calculation of PRH-Statistic Using Financial Revenue as Dependent Variable

*, **, and *** denote significance at 10%, 5%, and 1%, respectively.

c denote a rejection of null hypothesis at 1%.

J-statistic is the test for over-identifying restrictions in GMM dynamic model estimation.

AR(1) and AR(2)

During the period 2005–2017, the value of the H-statistic is 0.664. It indicates that total MFI revenue is earned in the market environment of monopolistic competition with more components of perfect competition. The estimated value of the H-statistic is found positive and significant but less than 1 during the period. This clearly rejects the chances of absolute monopoly or presence of perfect competition, which further gets confirmed from the Wald test at the 1 per cent significance level.

During the sub-period 2005–2011, the H-statistic is 0.724. It indicates that the microfinance sector was highly competitive during this period. However, the Wald test rejects the presence of perfect competition during the period. In the second half, 2012–2017, the H-statistic decreased to 0.306 reflecting a significant decrease in the competition level in the sector during this period. The structural transition of the microfinance market from highly competitive to monopolistic competition with more attributes of monopoly power is clearly visible.

The significant coefficient value of the lagged dependent variable displays partial adjustments towards equilibrium. The coefficients of all the three-factor inputs are positively significant for the whole sample period as well as during both sub-periods. It means any rise in the factor costs will lead to higher revenue. This indicates under-utilization of these resources. During the sub-period 2005–2011, the coefficient of interest expenses to GLP (WF) is highly positive and significant, contributing more than half in the H-statistic. This might be due to a decrease in the GLP of MFIs in the wake of the crisis during this period. The crisis compelled most of the MFIs to reduce their operations in the wake of rising loan defaults and political interferences.

With respect to control variables, the variable of credit risk, PAR30 is negatively correlated with the total revenue and found significant during 2005–2017. However, its value is found very low and insignificant during the sub-periods. The negative value of credit risk indicates that higher risk may lead to higher returns. The total assets (reflect the size of an MFI) have a positive and substantial impact on the earnings of MFIs. It shows that MFIs with large assets earn higher revenues. The coefficient of the capital-to-assets ratio is positive and statistically significant during the whole period, indicating that MFIs having access to equity capital may attain higher growth. However, its coefficient remains very low (negative during 2012–2017) and insignificant in both the sub-periods. The GDP growth, the macroeconomic factor, has a positive and significant effect on the revenue of MFIs for the whole period, though the value of its coefficient remains low. During the sub-period, 2005–2011, its effect is significant at 10 per cent significance level. However, during the period 2012–2017, its coefficient value is found statistically insignificant.

DISCUSSION OF THE RESULTS

The finding of the present study is consistent with the prior research on the association between competition and market structure. The rise in concentration in the Indian Microfinance market as reflected by the HHI index and CR ratios is accompanied by a decrease in the competition level in the market as indicated by the decrease in the PRH statistic. Competition and market structure in highly concentrated markets tend to be lesser competitive (Bain, 1951). An increase in the size of the firm increases the market power since the firm now holds a more dominant position in the market relative to its peers. However, a more modern and dynamic view states that competition may force firms to consolidate (Bikker & Spierdijk, 2009). This way, high competition ends up in a concentrated market.

Share of MFIs in Total GLP and Total Assets

Table 5 lists the top ten MFIs in terms of GLP for the years 2007 and 2011. Table 6 lists the top ten MFIs in terms of GLP for 2016. In 2007, four NGO/CU/Co-op MFIs were in the top 10 list with Cashpor being second in the list with the lowest profit margin. The combined share of the top 10 MFIs in total GLP is less than 20 per cent.

In the year 2011, the top 10 MFIs hold more than 72 per cent of total GLP. This year brought great turmoil in the Indian Microfinance market. The crisis which initiated in Andhra Pradesh (the A.P. Crisis) in 2010 soon affected the whole sector. The negative profit margin of MFIs depicts the severity of the crisis. Later, new regulations were introduced by the Government of India to make the sector more regulated. Some of the salient features of the new regulations are:

Creation of a separate category of NBFC-MFIs and bringing them under the direct jurisdiction of the RBI.

A margin cap and interest rate caps are imposed to protect the poor against any exploitation from MFIs.

The exposure limit for the individual borrower is set up to avoid chances of over borrowing and multiple borrowings.

Microfinance institutions are directed to establish a proper grievance redressal mechanism, mandatory enrolment to credit bureaus, and enforcement of code of conduct through industry associations (Srinivasan, 2011).

Microfinance institutions have to comply with the regulations laid down by RBI to get much-needed funds from banks under the priority sector.

Share of Top 10 MFIs in Terms of Total GLP in 2007 and 2011 (in %)

Share of Top 10 MFIs in Terms of Total GLP in 2016 (in %)

As the new regulations are more rule-based and incur high compliance cost, they favour big players to operate in the market. Furthermore, amendments in the rules regarding priority sector lending by banks have increased the interest of banks in having strategic alliances with financially strong MFIs as well as acquiring them (Sriram, 2016).

In 2016, the top 10 MFIs hold about 95 per cent of the total GLP with top three players holding more 50 per cent of the total GLP. The only NGO in the list is SKDRDP, holding 9 per cent of the total GLP without any change in the organizational set up. The interest cap set by the RBI under the new regulations kept the profit margin of MFI at a reasonable level. Except for Bandhan which is now a universal bank, the profit margin of the rest of the MFIs is between 12 per cent and 25 per cent.

Organizational History of the 10 Largest MFIs, 2016

Conduct and Performance of Leading MFIs

The current study finds that the Indian microfinance sector is highly concentrated with only 10 large MFIs holding about 95 per cent of the market in terms of GLP. The traditional economic theory finds high concentration favourable to earn supernormal profits. Although the structure of the financial market itself does not weaken competition (Bikker & Spierdijk, 2009), it indicates the possible threats to competition and exploitation of customers. The favourable structure of the market, market power, may create temptation for lenders to exploit the market. However, it is the conduct of the firms which is mainly responsible for the welfare or exploitation of the clients. Therefore, the study inspects the organizational history, key financial and social indicators, the interest charged and outreach of the MFIs, in order to examine the conduct of these MFIs. Such examination becomes more critical as the marginalized section of the society is the main target market of the sector.

Organizational History

The examination of the organizational journey of the MFIs since inception provides vital clues about the chances of possible mission drifts.

8

Mission drift is defined as MFIs losing their original mission, that is, their focus on the poor and, moving up market (Copestake, 2007).

In Table 7, a brief organizational history of the 10 largest MFI is presented. The role of the original promoters of the MFIs in managing the affairs of the organization is also presented.

It is found that most of the MFIs initiated their operations as NGOs. Later, they got transformed into NBFC. The MFIs are now either working as banks or on the verge to convert into banks. Although original promoters are still with their MFIs, conversion of MFIs into banks is a significant change. Microfinance caters to the underserved sections of society, and therefore, the difference between banking and microfinance is worth preserving.

Financial Indicators

Interest rates charged by the MFIs are one of the major concerns for policymakers all around the world. Although microfinance disregards the risk-return trade-off, the high operating costs compel MFIs to charge a higher rate of interest in comparison to mainstream banks. The presence of commercial borrowings and private equity further increases the pressure on MFIs to earn more. However, charging high interest rates defeats the basic objective of microfinance.

Various reports indicate that the lending rates of MFIs have come down since 2010. (Misra, 2016). After the AP crisis, the RBI has put a cap on lending rates of MFIs to protect the interests of poor borrowers. As per Microfinance Institutions Network (MFIN) report, the pricing on the majority of the portfolio across MFIs ranges from 19.8 per cent to 27.2 per cent, which is well under the prescribed margin cap (MFIN, 2016) It is found that the interest rates of larger MFIs decrease with the rise in their GLP (MFIN, 2016). This trend reflects efficiency gains. This proves that though the top 10 MFIs are giant players, they are not trying to earn supernormal profits. On the other hand, the smaller MFIs are charging a higher rate of interest in comparison to large and medium MFIs (Misra, 2016). This might be due to high operating and financing cost.

Social Performance Indicators

One of the important indicators of measuring social performance of MFIs is its outreach.

9

Outreach is the expansion of credits and other financial services to the wider and poorer of the poor (Conning, 1999). It has two aspects: breadth (total number of clients) and depth (how far poorer of the poor or less privileged served by an MFI).

After reviewing the outreach performance of the top 10 largest MFIs, it can be concluded that the leading MFIs have achieved growth in their business mainly by increasing the breadth of their outreach and the loan amount of existing clients. Moderate growth in the loan amount per borrower is healthy as it indicates upliftment in the life of the client. However, rapid growth in it indicates that MFIs are targeting better-off clients ignoring the poorer clients. As per Sa-Dhan (2016), the business models of MFIs have become more urban-centric. The steep hike in average loan balance per borrower also affirms this finding.

CONCLUSIONS

The results of the empirical investigation find a rise in concentration with a decrease in competition level in the Indian microfinance market during recent years. It resembles a monopolistic form of the market with the features of a monopoly. The study finds high competition level in the first sub-period; however, the competition level has decreased in the post-crisis period. The study finds that after the introduction of rule-based regulations, the sector has further consolidated. High concentration gives large firms market powers, which can be exploited to earn more profits by charging high-interest rates on loans. However, the study fails to find evidence of any such attempt to exploit the market power from the conduct of the leading MFIs.

As a policy implication, the study highlights the possible link between the fall in the competitiveness of the sector with the introduction of new regulations in light of the sectoral crisis. The leading MFIs have registered spectacular growth holding a major share of the market. It is required that the regulators keep a close watch on the operations of such MFIs and take necessary actions to preserve a healthy competitive environment in the sector. Furthermore, existing rules should be modified to help small MFIs, as they play a very crucial role in the accomplishment of the primary objective of the microfinance. Many MFIs are tempted to become full-fledged banks. The difference between microfinance and mainstream financial services should also be preserved as the beauty of microfinance mainly lies in its distinctive features with respect to traditional mainstream banking.