Abstract

Keywords

Capital accumulation, when considered as a geographical process from the very start, tends to produce distinctive urban regions within which a certain structured coherence is achieved and around which certain class alliances tend to form. – Harvey (1985: 156)

Existing VC [venture capital] studies in geography are predominantly on North America and Western Europe, and the focus has been on the spatial operation of mature VC firms in established VC centers, rather than on the formation of new VC funds and centers. – Zhang (2011: 1562)

Introduction

The process of capital accumulation has been premised on and driven through urban regions. This phenomenon intensified after WWII through state spatial strategies to attract capital to strategically selected cities. Herein lies a dynamic logic at work: urban regions have become key platforms for the reproduction of capital, but political leaders at multiple levels must also consistently create attractive conditions for these regions to secure capital investments. To Harvey (1978: 113), this pro-accumulation approach constitutes the

Emerging research suggests more need to be done on top of regularly re-assessing the evolution and mutation of urban entrepreneurialism (He, 2020; Wu, 2020). As Phelps and Miao (2020) demonstrate, the urban process of capital accumulation now includes specific characteristics known as urban diplomacy, namely efforts to brand, market and promote cities, and urban intrapreneurialism, namely innovation and invention within public organizations to enhance the capital accumulation process. Yet these new characteristics may be insufficient for driving growth. Urban entrepreneurialism, Phelps and Miao (2020: 314, emphases-in-original) explain, has engendered a distinct feature known as ‘urban speculation’, namely ‘the way in which national and local governments are complicit in what could only be regarded as forms of

These observations are highly germane to the debates on the limitations and future potential of urban entrepreneurialism to the urban process of capital accumulation. Specifically, they reinforce Peck's (2014: 399) argument that Harvey's conceptualization of urban entrepreneurialism ‘provides a critical benchmark of sorts against which subsequent transformations can be evaluated’. At the same time, however, the

Addressing this question is highly pertinent within a contemporary global economy wherein competitive strategies have moved

Crucially, the state's role as a direct investor in the urbanization process is not an historically novel development that is only emerging in the current conjuncture. As this paper will show, state institutions proactively launched venture capital (VC) investments to drive urban growth and development since the 1950s. Understanding the emergence and evolution of state-driven VC (hereafter SVC) investments could offer a concrete avenue for examining the state's overlapping roles in the urban process of capital accumulation. In turn, it calls for a re-assessment of what Alami and Dixon (2023: 87) term ‘the deep-seated capitalist transformations which have fundamentally underpinned the historic arc in the trajectories of state intervention on a global scale’. A crucial transformation is the integral role of SVC investments in the urban process of capital accumulation – a role this paper conceptualizes as urban state venturism.

Urban state venturism refers to the transposition of state institutions into venture capitalists to strategically select and finance firms with innovative potential in targeted urban regions. National governments have played a significant role in bolstering their respective domestic VC markets through interventional tools such as tax credits, regulatory changes and, as this paper will elaborate, state-led VC investments.

1

These tools collectively constitute what Klingler-Vidra (2018) terms a VC state that both creates conducive business environments for private VC firms

This paper builds on this expanding – and potentially most ambitious – aspect of urban development through presenting a new research agenda on the state's existence as Why have state institutions chosen to become VC investors in targeted urban regions and firms despite high commercial risks? How would the distribution of profits and losses shape the economic development of urban regions? Do these speculative investments represent an emergent form of urban state developmentalism, or are they actually more risk-laden expressions of debt-fueled growth?

This agenda connects two major fields of research in geographical political economy: urban economic development and ‘new’ state capitalism. First, it will add new dimensions to the prevailing conceptualization of the urban process under capitalism. For Harvey (1978: 124), this process is a way in which ‘Capital represents itself in the form of a physical landscape created in its own image, created as use values to enhance the progressive accumulation of capital’. Yet, when the state's role as capital is conceptualized as

The subsequent discussion will be organized in four parts. The next section will re-conceptualize the urban process of capital accumulation by focusing on one specific aspect – the evolving and multi-dimensional role of the state. In doing so, the section highlights how the state's function as capital becomes imbricated with both firm-level drivers of capitalist urbanization and ‘entrepreneurial’ initiatives that facilitate this urbanization. The third section will discuss the emergence and evolution of urban state venturism. It posits this phenomenon as multi-scalar state developmental initiatives that are not simply superimposed on but are actualized through urban regions. Three future research directions that critically assess the rationale and effects of urban state venturism will be presented in a new research agenda in the fourth section. The contributions of this agenda to debates on urban political economy will be addressed in the conclusion.

Reconceptualizing state involvement in the urban process of capital accumulation

The urban process of capital accumulation has engendered a plethora of state initiatives to create conducive conditions for investors. As Logan and Molotch (2007: 49) demonstrate in their seminal book,

These conceptualizations underpinned subsequent explorations of state involvement in the urban process of capital accumulation. ‘To understand specifically how urban entrepreneurialism emerges’, Wu (2018: 1384) argues, ‘the changing role of the state in governing urban transformation should be contextualized with appropriate attention to particular institutional settings’. Working across the variegated contexts of Chinese cities, Wu (2018: 1394) develops a concept of ‘state entrepreneurialism’ to accentuate the role of ‘planning centrality’, through which state institutions ‘modify, change and adjust its governance practices’ to facilitate capital accumulation. Also focusing on how state institutions proactively shape the urbanization of capital is Brenner's (2004, 2019) work on the production of new urban spaces through state spatial strategies. As Brenner (2019: 11) puts it: New urban spaces have been actively forged through the aggressive, and often socially and politically regressive, rescaling of state space during the last four decades [i.e. since the 1970s]. More specifically, the production of neoliberalized regimes of urbanization has occurred in large measure through spatial and scalar transformations of statecraft that have extended, institutionalized, and normalized market discipline across the urban fabric while also targeting certain strategic sites within each territory for intensified transnational investment, advanced infrastructural development, and enhanced global connectivity.

To follow Peck and Whiteside (2016: 237), financialization is ‘a historic process of systematic financial intensification, which is reflected, inter alia, in an increased reliance on (and resort to) financial inter-mediation and financial engineering, along with a host of financial logics, metrics, and rationalities’. Non-financial firms have consequently increased their involvement in financial market transactions while municipal governments are incentivized to collateralize land for bond issuance. Underpinning financialization is a specific outcome of state strategies that prioritized deregulation in financial markets – the debt machine. Debt-machine strategies have been implemented to finance urban governance and reshape the governing rationalities of US cities such as Detroit and Chicago within a broader national context of slow economic growth (Peck and Whiteside, 2016; Weber, 2010). Key characteristics of these strategies, Peck and Whiteside (2016: 263, original emphasis) demonstrate, are ‘invasive processes of financial colonization, often realized at the nexus of bondholder-value pressures and

Similar impacts of debt-machine dynamics have emerged in Europe. In Paris, France, the local authority has limited financial capacities to complete mega urban redevelopment projects and must rely on private sector developers that operate in line with the demands of modern portfolio management (Guironnet et al., 2016). Examining urban regions across France, Wijburg (2019: 209) shows how ‘the French state has created a financialized urban governance regime in which REITs, of which one is publicly owned, exercise considerable autonomy’. Through in-depth interviews with more than 50 key actors in municipal governance and the finance industry across England, Pike (2023: 9) shows how financialization has permeated local statecraft to the extent that financial innovation is now construed as ‘a potential fix for local governments facing fiscal stress’, in turn triggering ‘the emergence of new and complex financial ideas and instruments alongside weakened local transparency, scrutiny and accountability’.

Perhaps the most unlikely expression of the debt machine is its impact across fast-urbanizing China following the turn to market-like rule during the 1980s. While the Chinese financial system remains relatively insulated from the global financial system, its fundamentals have been modelled on financial practices worldwide that, in many aspects, enabled deepening connections with global financial centers. What is unique to the Chinese urbanizing context is the

Involving myriad coalitions of real estate developers, banks, local governments, and retail stock investors, this speculative and rent-seeking approach to urban development in China has been widely described as ‘land-leverage-infrastructure’ (Tsui, 2011), ‘rolling development’ (Jiang and Waley, 2020), or simply, land financialization (Wu, 2023). These developments collectively reflect how urban financialization has become a global phenomenon today. The rationale may differ within the Chinese political economy where local governments confront colossal structural pressure to generate extra-budgetary funds, but the method on and desired outcome of urban development are identical: value creation through place-making and/or real estate projects that are largely underpinned by debt and are unconnected to non-financial industrial competitiveness.

What the foregoing empirical evidence reveals is

Expressed in Figure 1, the framework considers the possibility that this urban process can be constituted by capitalist urbanization

The state as capital in the urban process of capital accumulation.

State-driven VC investments are entwined with the urban process of capital accumulation partly because urban regions have been long-standing centers of capital accumulation and partly because innovative start-ups tend to locate in urban regions and possess the potential to become unicorn companies 3 and/or global market leaders. As the next section will elaborate, the state's role as a direct investor in VC markets is not an historically novel phenomenon. Indeed, SVC investments have existed for several decades in tandem with emergent neoliberal regimes of urbanization. Understanding the evolution of these investments and their manifestation in urban regions is therefore important for exploring the growing contributions of urban state venturism to global-scale uneven and combined urban development (see the top of Figure 1). These contributions then generate new impetuses for state institutions to devise state spatial strategies and drive capitalist urbanization.

The emergence and evolution of urban state venturism

Equity investments by VC investors have become an important tool to finance high-risk commercial projects after WWII. Equity differs from debt because it does not require a pre-specified rate of return within a fixed time period and remains flexible in response to future strategic adjustments (Inoue et al., 2013). Investors can provide the necessary support to ensure that selected firms can succeed at different stages of production – from the formulation of initial ideas to pilot products and, finally, market share capture. Fundamental to this support is the generation of economic returns through

The first true VC firm, American Research and Development, was established in 1946 by then MIT President, Kal Compton, together with Georges F. Doriot and local business leaders in Boston (Gompers and Lerner, 2001). The VC industry subsequently grew in the US and flourished in the 1990s, with investments concentrated in information technology industries, mostly in California, New England, and the Great Lakes. A defining characteristic of these investments is strong innovative potential. On average, Gompers and Lerner (2001: 165) estimate, ‘a dollar of venture capital appears to be three to four times more potent in stimulating patenting than a dollar of traditional corporate R&D’. Between 1983 and 1992, for instance, VC investments accounted for less than three percent of corporate R&D, but was responsible for about 10 percent of US industrial innovations, giving rise to what Gompers and Lerner (2001) call the VC revolution.

A significant but relatively under-focused point in the US context is the importance of Federal Government support for VC investments in technological innovation and marketization (see Table 1). Even the rise of Silicon Valley, an industrial region in the south of the San Francisco Bay Area that is widely recognized as the global beacon of VC investments, was an outcome of substantial support from US government policies (Klingler-Vidra, 2018). As Weiss (2014) demonstrates, research grants, regulatory changes, and tax credits introduced by US governmental agencies contributed directly to the success of the American technology sector in Silicon Valley. Many national governments subsequently attempted to build their own VC markets with an explicit aim to emulate the high-profile global success of firms from Silicon Valley. Klingler-Vidra (2018) observes at least 45 countries have harnessed public policies to foster their own Silicon Valley-like VC markets to boost innovation and entrepreneurship. This combined emergence of SVC investments across and beyond US urban regions reflect how state initiatives directly benefit from and in turn determine uneven and combined urban development.

Public venture capital initiatives in the United States, 1958–1997.

One major example of adaptation is found in New York City. In 1991, the New York City government created the New York City Economic Development Corporation (NYCEDC) as its primary platform to promote strategic sectors that included bioscience, media, and the Internet communications. The NYCEDC supports startups and offers infrastructure to high-tech firms in the city by negotiating growth-oriented deal structures through its Strategic Investments Group (SIG). Managing a US$180M + aggregate fund portfolio that invests across a variety of sectors, including real estate, VC, energy, and infrastructure, the SIG is pivotal in ‘improving access to finance for underserved groups and catalytic investment capital to strategic sectors’ (https://edc.nyc/finance-solutions). This portfolio includes the Industrial Development Loan Fund, the Not-for-Profit Loan Fund, the Early Stage Life Sciences Fund 1 and 2, the LifeSci Expansion Fund, the Emerging Developer Loan Fund, the Neighborhood Credit Fund, WE Venture, and WE Fund Credit. Fundamentally, NYCEDS is tasked to implement a city-level industrial policy that enables the growth of innovation districts (Zukin, 2021), a task it fulfills through urban state venturism.

VC was adopted and promoted by European state institutions in direct response to US private VC hegemony. Business development and growth are explicit objectives of European SVC investors (Grilli and Murtinu, 2015). Some well-known SVC investors include Biotech Fonds Vlaanderen in Belgium, SITRA in Finland, CDC Innovation in France, Axis Participaciones Empresariales in Spain, and Scottish Enterprise in the UK. The allocation of fiscal funds to SVC investments includes three main modes: direct public funds, hybrid private-public funds, and funds-of-funds (Block et al., 2018). The main goal of establishing SVC investments is to alleviate the regional disparity in financial investment and pursue projects that can yield positive social benefits. These investments were similarly established in Asia's newly industrializing countries to drive economic growth at different scales. During the 1990s, the growth of high-technology industries in Israel, Singapore, and Taiwan has been attributed to SVC initiatives (Lerner, 2000).

SVC investments grew substantially across China after the municipal governments of Beijing, Shanghai, and Shenzhen began launching VC investments to guide local high-tech industries and invest in innovative start-ups (Miao, 2018; Zhang, 2011). For instance, Shenzhen Capital, established by the Shenzhen city government in 1999, has achieved results that are comparable with top private VC firms such as IDG Capital and Sequoia Capital. It is now ‘a comprehensive investment conglomerate major in VC/PE with registered capital of RMB 10 billion [∼US$1.44 billion] and total asset under management of approximately RMB 423.9 billion [∼US$61 billion]’ 4 Among Shenzhen Capital's 972 recorded investment projects, portfolio firms are mainly located in Shenzhen (253), Beijing (131), and Shanghai (86). 5 In Shanghai, the municipal government first established Shanghai Venture Capital Co. in 1999 to support high-tech firms before subsequently launching the Venture Capital Guiding Fund of Shanghai in 2010 and the Shanghai Angel Capital Guiding Fund in 2020 to collaborate with private VC firms. The latter guiding funds are financed by the Shanghai municipal government with a clear goal to shape ‘the flow of private funds into key industrial fields in Shanghai, especially in strategic emergent industries’. 6

An overview of key SVC investments in selected economies beyond the US is presented in Table 2. This overview is not comprehensive, to be sure, and does not exhaust the variety of state venturism in different geographical contexts. What the paper seeks to highlight is the

Major government venture capital funds in the UK, Canada, and China.

First, the state and capital have been construed as ontologically separate entities. Existing research on state-driven initiatives predominantly focuses (a) on how urban authorities build partnerships or alliances with private investors (Austin and McCaffrey, 2002; Goldstein and Mele, 2016), and (b) on a narrow range of projects such as place marketing and land-based urban regeneration and gentrification (Holmes, 2022; Lees, 2022). Less known are the ways in which SVC investments are launched within and across different urban contexts. Second, SVC investments could be positioned

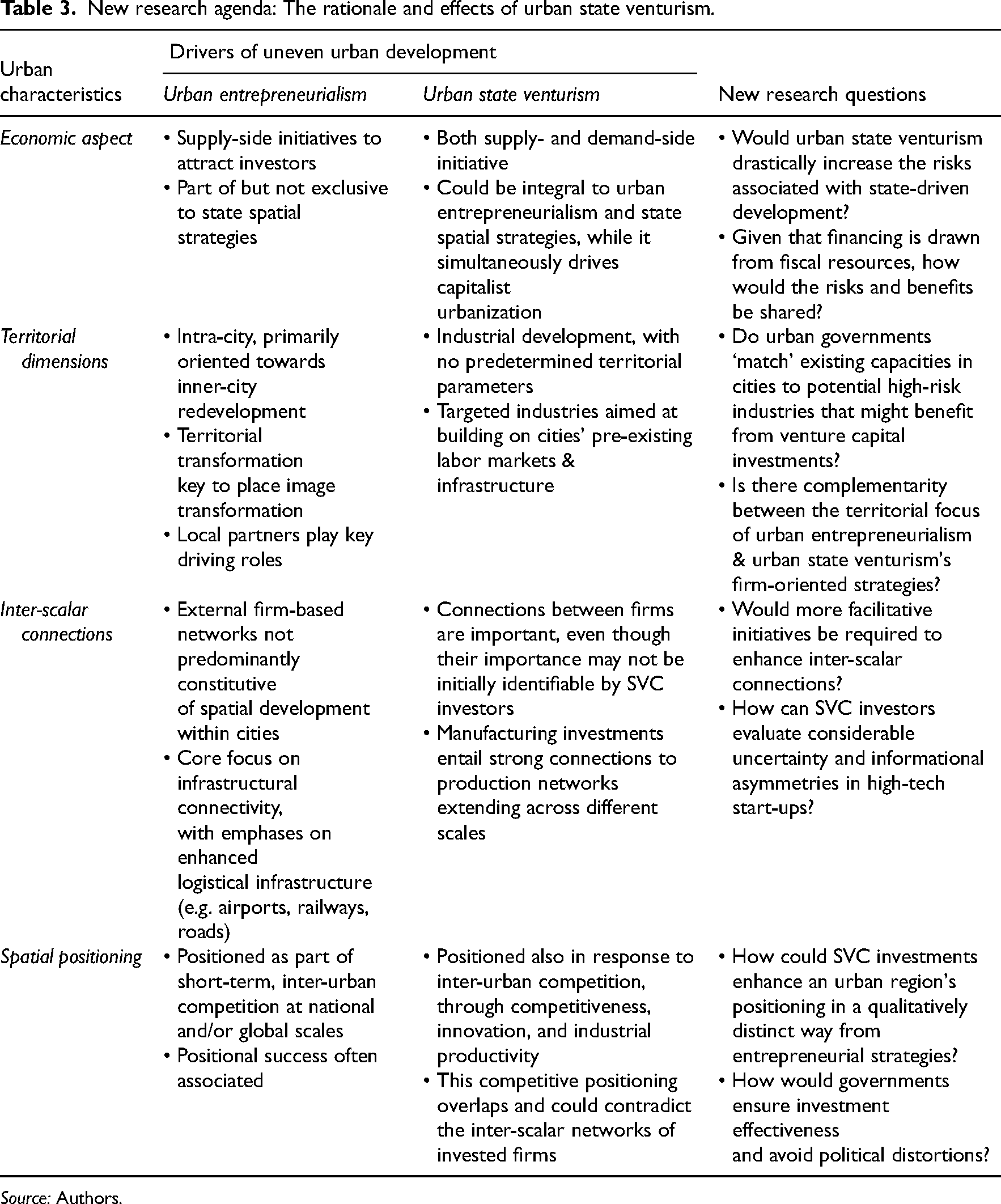

Urban state venturism: A new research agenda

The emergence of urban state venturism highlights at once the Why are urban governments emulating the private VC logic of high-risk investments? How are profits and risks defined and redistributed when urban governments drive innovation and economic development through VC investments? Is urban state venturism a form of ‘developmentalism’ that characterized the rise of East Asian developmental states, or is it simply a more extreme version of the debt machine?

The rationale of high-risk urban state ventures

Speculative urban investments have proliferated globally alongside the consolidation of neoliberal capitalism after the 1970s, but the

First, private VC investors develop a very narrow band of technological innovations that could potentially generate high and rapid economic returns. The time frame for redemption by fund providers, usually five to ten years, means these private investors prioritize investment opportunities that can realize value through successful exits within this relatively short period. Second, a small number of private VC investors shape the geographical concentration of investments in technological change and could affect the geographical spread and impact of spinoffs. In the United States, three urban regions – the San Francisco Bay Area, Greater New York, and Greater Boston – account for about two-thirds of VC investments deployed by firms each year. Similarly, the Chinese city-regions of Beijing, Shanghai, and Shenzhen account for over 70% of all VC investments (Pan et al., 2016; Yang and Zhu, 2023). The concentration of these investments in a small number of major urban regions suggests VC investments may not be a universal developmental tool for other urban regions without strong state involvement. Third, a relative lack of emphasis on corporate governance and management skills exposes VC firms to higher risks once firm founders fail to secure steady revenues after investing substantial sums of money. In addition, VC firms charge fees high enough to impel public investors to invest

The discursive justifications of risky VC investments by state institutions offer an avenue to examine the rationale of these investments. Juxtaposed against these justifications are claims of SVC investors’ operational inefficiency. To Florida and Kenney (1988), public equity funds possess limited potential in VC networks by public equity funds. While some SVC investments can succeed in financing high-tech firms in cities where private VC resources are

There are at least three plausible reasons. First, SVC investments could boost national competitiveness in strategically selected high-value sectors. For instance, the Small Business Investment Company (SBIC), one of the pioneering SVC firms in the US, contributed substantially to VC investment infrastructure after its launch in 1958 vis-à-vis criticisms of its low financial returns and fraud associated with some funds (Lerner and Watson, 2008). Notwithstanding these criticisms, Lerner and Watson (2008: 8) explain, the officials in charge persisted with the program and their commitment paid off when the SBIC went on to stimulate ‘the proliferation of many venture-minded institutions in Silicon Valley and Route 128 – the nation's two major hotbeds of venture capital’. The profit-making goals of portfolio firms may not be achieved most efficiently, but the socio-political goal of a dynamic VC market in the selected urban regions was achieved successfully. Of particular interest is whether urban governments are uniformly justifying VC investments based on broader socio-political goals. If so, the identification of these goals would further enhance knowledge on the rationale of urban state venturism.

Second, SVC investments offer a relatively faster way that

Finally, SVC investments can contribute to rebalancing urban development across state territory (see Figure 1's focus on the imbrication of state facilitation and investment). As Vogelaar and Stam (2021) demonstrate, state economic involvement through SVC investments is not confined to fixing market failures; rather, Dutch provinces intervene in the regional VC market because provincial governments emulate others in new development policies and are even impelled to maintain local competitiveness through SVC investments. During the 2008–2012 and the 2013–2017 periods, Vogelaar and Stam (2021) reveal, over two-thirds of all private VC investments were concentrated in three highly urbanized provinces: Utrecht, Noord-Holland, and Zuid-Holland. Meanwhile, rural provinces in Holland lag far behind in terms of private VC investments. This regional disparity demonstrates how private VC is primarily driven by economic vibrancy and profit returns, two dimensions closely associated with economically competitive cities such as Amsterdam and Rotterdam.

A contrast between the number and value of portfolio firms provides further insights into the role of VC investments as

The distribution of risks and profits

One major issue pertaining to urban entrepreneurialism – and, more broadly, state spatial strategies targeted at urban regions – is the disproportionate concentration of profits in businesses and, conversely, the disproportionate impact of losses on the taxpaying public. Whether urban state venturism generates similar challenges spotlights power imbalance between different stakeholders. As this paper has argued in the second section, state roles need not be confined to market regulators or passive partners of private investors in urban (re)development: state-linked institutions can also assume direct risks

Four aspects of profit generation and redistribution via urban state venturism require further attention. First, how state institutions develop the monetary and professional capacities to invest in, oversee, and evaluate high-tech startups. Second, how high-tech and high-risk innovative firms are identified and selected by SVC investors. Third, how SVC investors compete and/or cooperate with private investors in the identification of investment targets. Last, but not least, how or whether profits generated from successful exits would be reinvested into socially progressive programs. Research on these four aspects would advance knowledge on the operationalization of SVC investments and, in turn, provide data for evaluating their effectiveness

Like their private counterparts, SVC investments are fraught with risk and their governmental linkages do not guarantee better portfolio returns. For instance, in Wuhan, a major city in central China, local governments invested about CNY 200 million (∼US$30 million) in Wuhan Hongxin Semiconductor Manufacturing Co. for a 10% equity stake. In addition, these governments offered public subsidies to Hongxin in 2018 and 2019, but the corporation failed abjectly even before it started to manufacture chips in 2020. All Hongxin-related VC investments by local governments in Wuhan morphed into a real loss. 8 This example of a failed SVC investment demonstrates how, in a high-risk market, state authorities (and therefore the taxpayers) could easily be exposed to substantial losses.

Indeed, the common failure to generate successful exits in many SVC projects raises a question on the definition of risks: are risks only ascertained based on profits, or do SVC firms incorporate other factors in their risk assessments? Political leaders in charge of these investments may have their accomplishments evaluated through non-profit metrics, such as their ability to establish strategically important industries that could augment urban development in ways that are both tangible (e.g. income, employment, increased logistical flows) and intangible (e.g. attracting high-quality workers, stimulating place-specific competitiveness through new firm formation).

Research has identified a difference between private VC investors, who prioritize profits, and SVC investors, who work towards generating positive social impacts that transcend the maximization of efficiency and profit (Block et al., 2018; Johansson et al., 2021). For instance, Block et al. (2018: 243) observe that SVC investors aim to ‘alleviate the financial gap problem as well as the same time to pursue investments that will yield social payoffs and positive externalities to the society’. For this reason, state institutions tend to possess different tolerance zones vis-à-vis private VC firms. As Avi Hasson, Israel's chief scientist and a former venture capitalist, puts it in a 2014 presentation, ‘governments are more tolerant of real risk than venture capitalists can be’ (cited from Klingler-Vidra, 2018: 418).

While more real risk tolerance could engender more speculative investments, this is not an intrinsically negative approach. Writing about the effectiveness of industrial policies, Rodrik (2010) argues that what distinguishes good performance from bad performance is not the presence or absence of these policies but the

Beyond focusing on individual cases within urban regions, the question of risks and benefits could also be addressed in terms of urban regions’ spatial positioning within the global system of capitalism. Existing evidence suggests urban state venturism actively leverages innovative ideas, high technology, and finance to create a new ecology of economic development that benefits a very small number of urban regions, or so-called VC centers, at the heart of the global economy and further sidelines those urban and national institutions that cannot cultivate such an ecology for high-tech startups (Chen et al., 2010; Pan et al., 2016). Inevitably, urban state venturism exacerbates domestic and global uneven development and economic polarization (see Figure 1). These outcomes raise questions about how real benefits from SVC investments in booming high-tech sectors can be distributed across the globe and whether the accompanying risks will be sufficiently serious to generate systemic crises. The challenge, as Harvey (1985: 159) presciently identifies nearly four decades ago, could rest in the political-economic power amassed by the ruling class alliance comprising both state and non-state actors: The political power of a ruling class alliance is not confined to an urban region: it is projected geopolitically onto other spaces…The power that a ruling-class alliance projects depends in part upon the internal resources it can mobilize. Financial and economic leverage is crucial. This in part depends upon the urban region's competitive position. But competition is not always between equals: urban regions with enormous and complex economies cast a long and often dominant shadow over the spaces that surround them…Those urban regions, like New York and London, which command power within the realms of credit and finance (the central nervous system of capitalism) can use that power across the whole capitalist world.

Urban state venturism as urban state developmentalism?

The transposed role of SVC investors at the urban level exemplifies a

The ‘developmental state’ concept gained popularity following Chalmers Johnson's (1982) research on Japan's post WWII economic resurgence. This state formation comprises a specific institutional ensemble of planning, operations, and strategies that support domestic firms in mediating and combating competition in the world market. A core approach of the developmental state is to create conducive environments that nurture ‘national champions’ (i.e. global leading firms), an approach that corresponds with the overarching aim of urban state venturism to produce new ‘champion’ firms to drive urban development. Yet the ‘classic’ prototype of East Asian state developmentalism is one that reflects a key issue identified earlier in this paper – the dichotomous distinction between the state and capital, such that the state is embedded in society with the aim of enhancing social well-being while simultaneously remaining autonomous from capital (Evans, 1995; Johnson, 1982). Adding to this issue is the widespread state-centrism of research on developmental states that largely overlooks processes occurring at the subnational levels. An open question on urban state venturism, then, is what developmental philosophy is adopted by state institutions in a way that

Crucially, this question is applicable to urban regions beyond East Asia. As Block (2008) demonstrates, the US Federal government's interventions to support the national innovation system and private high-tech firms exemplify a ‘hidden developmental state’. ‘Consistent with ideas of the ‘knowledge economy’ or postindustrial society that stress the economy's immediate dependence on scientific and technological advance’, Block (2008: 170, original emphasis) asserts, ‘governments have embraced developmental policies that support cutting edge research

State developmentalism in East Asia currently encompasses the use of VC investments as strategic tools. Public policies and funding in Hong Kong, Singapore, South Korea, and Taiwan have been harnessed to foster VC markets through start-ups and high-tech innovation. Despite their variegated strategies, three general policies have been introduced that correspond with what Klingler-Vidra (2018) terms the ‘venture capital state’: investing in start-ups through private VC partners, improving national regulatory environments related to innovation and entrepreneurship, and providing tax breaks. They reflect, specifically, Klingler-Vidra's (2018: 389) observation that ‘more state involvement, not less, has propelled the global spread of a supposedly archetypal manifestation of laissez-faire: venture capital’. This paper adds to Klingler-Vidra's (2018) conceptualization by considering state institutions’ role

State institutions at different administrative levels across China are creating various state-funded Industrial Investment Funds (IIFs) to channel investments in urban regions. One of the biggest IIFs in China is National Integrated Circuit Industry Investment Fund Co., Ltd. Created in 2014 by the Ministry of Finance and other state funds, this IIF raised funds in two phases. Phase I generated 138.7 billion yuan (∼US$19.9 billion) and Phase II, launched in 2019, raised a further 200 billion yuan (∼US$28.7 billion). By the end of 2021, over 1400 state-guided or state-funded IIFs valued collectively at 2386 billion yuan (∼US$342.2 billion) were established across China, of which over 80 percent were created by municipal governments (Liu et al., 2022). Under the Interim Measures on Managing State-funded IIFs introduced by the Chinese National Development and Reform Commission in 2016, IIFs must serve as funds of VC funds, and government investors are not allowed to participate in the daily operation of fund managers or fund custodians. In reality, however, many IIFs created by municipal governments act as VC firms that invest directly in portfolio firms that could potentially contribute to the attainment of developmental goals.

In Singapore, the Infocomm Development Authority in 1996 created Infocomm Investments Private Limited (IIPL) as a wholly owned subsidiary to promote VC investments. Unlike private venture capitalists, IIPL works to support and complement state efforts to build a globally competitive Infocomm industry in Singapore. In 2015, IIPL launched a new initiative – Building Amazing Startups Here – to provide all-in-one startup facility to build an ecosystem of start-ups and tech companies (

Two specific characteristics can be discerned from these examples to distinguish urban state venturism from conventional East Asian state developmentalism. First, the venturist approach is much more firm-focused (i.e. it targets specific firms with prodigious potential and seeks to attract them to drive innovation and entrepreneurship in targeted urban regions). Second, the state is transposed into a capitalist through its VC investments (hence the state

Whether urban state venturism represents a speculative extension of state developmentalism requires further research because it would illustrate why and how states handle the limits to ‘entrepreneurial’ policies (see the introductory section). Indeed, if urban state venturism entails what Miao and Phelps (2019) call state intrapreneurship in guiding industrial priorities, then this guiding process is not confined to innovating new plans and policies; innovation must also encompass ascertaining and investing in firms to realize these priorities. Because state capacities and regulatory objectives differ, the ability and willingness to exploit the opportunities of VC are more apparent in some economies such as China, the US, and the EU than in others. The key question here is whether existing conditions, both political and economic, would enable urban governments to shape developmental outcomes through VC investments.

Towards a dynamic research agenda on urban state venturism

The foregoing three-pronged agenda raises fresh questions about the rationale and impacts of urban state venturism. In line with Figure 1, the overarching goal of this agenda is to stimulate debates on the urban process of capital accumulation through SVC investments. It presupposes the production and

New research agenda: The rationale and effects of urban state venturism.

Undoubtedly, considerable empirical investigation is needed to articulate the dynamic aspects of urban state venturism and analyze how much it can promote high-tech sectors and enhance urban competitiveness. This simultaneously engenders new research opportunities and challenges, particularly in cross-national comparison. However, through highlighting varying degrees of state involvement in VC investments, from low-risk regulatory changes to high-risk direct investments, this agenda enables more fine-grained discussions on the imbrication of state spatial strategies, of which urban entrepreneurialism is a key manifestation, with capitalist urbanization, a process that augments demand for goods, amenities, and services (see Figure 1). Institutional rules and capability ranging from tax regulations and funding supply to investment mandates and risk bearing shape the uneven approaches to generate innovation and entrepreneurship in urban regions. Here is where the facilitative aspect of state institutions becomes pronounced in shaping capitalist urbanization through SVC investments. Understanding urban state venturism in different geographical contexts entails an analytical focus on the continuity and transformation of the state's roles

Conclusion

‘[C]ities can and should participate directly in the venture-capital world by tapping into the ebullient energy of urban startups. These firms are developing disruptive, scalable solutions to some of society's trickiest challenges, including housing, mobility, logistics, food production, water treatment and renewable energy’.

Innovation…calls for venture capital and specific labor skills in its development, access to distribution systems for marketing, and openness on the part of recipients which may entail the redesign of consumer markets and the transformation of taste and fashion.

– Harvey (1985: 157)

This paper has spotlighted urban state venturism as an entry point for evaluating the overlapping roles of the state in the urban process of capital accumulation. States facilitate capital accumulation in urban regions through spatial strategies that cater to the demands of capitalists, yet they also generate these demands

In this regard, urban state venturism can be conceptualized as an extension of urban entrepreneurialism. Both approaches speculatively promote what Brenner (2004: 16) calls the ‘localized territorial competitiveness’ of particular territories within a national and/or global context. At the same time, however, urban state venturism has been less, if at all, about land-based (re)development, place marketing and/or infrastructural provision for privately oriented development projects; it is more about state-linked institutions’ deployment of VC investments to achieve three distinct but interrelated objectives: enhancing urban regions’ economic competitiveness through establishing more high-tech firms, generating higher returns on public surplus capital, and rebalancing urban and regional development.

These developments collectively complement and complicate Schindler et al.'s (2023) critical evaluation of the so-called ‘Wall Street Consensus’. Under this new accumulation regime, state authorities allow greater space for private market actors to shape developmental outcomes and correspondingly undertake less risks (i.e. the state provides ‘de-risking’ support for private actors). While urban state venturism exemplifies the state's embrace of market regulatory logics, it marks an increase in capital investments

An additional research question that would be of immense policy relevance is whether the pursuit of state objectives through urban state venturism places residents of participating cities at greater economic risks. Indeed, if residents/citizens are expected to bear the costs of failure, how socially