Abstract

Keywords

Introduction

This study aims at analyzing the relationship between new venture survival, and the social context(s) of entrepreneurial teams and founding team gender diversity. In this task, we employ a unique, prospective longitudinal database comprising a large number of Swedish ventures established in 7 different years in the first half of the 20th century and in the early 21st century. The study sets out from the established conception that venture performance is a context-specific outcome at several analytical levels, as well as dependent on time (Aldrich, 2009; Welter, 2011). We ask if there is a difference in the likelihood of survival for ventures founded by an entrepreneurial team, as compared with ventures founded by solo entrepreneurs. Moreover, we ask if the probability of venture survival is affected by the ventures’ founding constellation with regard to gender. As gender is an integral phenomenon in our study, we also ask whether this relationship has changed over time.

Team entrepreneurship, gender structures, and the context of entrepreneurship have received increasing attention (Holmquist & Carter, 2009; Welter, 2011). Scholars have since long claimed that multiple analytical levels have the potential to provide important insights (Davidsson, 2008; Low & MacMillan, 1988). In particular, the entrepreneurial team is considered to be a promising framework of analysis. In spite of this, teams have gained relatively little attention in the past research (Cooney, 2005; Cooper & Daily, 1997; Davidsson & Wiklund, 2001; Martinez, Yang, & Aldrich, 2011), and there are few large-sample studies on the performance differences between solo start-ups and team start-ups (Gueguen, 2013). The need for a more explicit highlighting of the entrepreneurial team, as well as an exploration and evaluation of earlier theoretical contributions and their applicability, is considered to be urgent (Aldrich & Kim, 2007; Larsson Segerlind, 2009; Zhou & Rosini, 2015). In particular, this concerns the question of gender differences in the initial formation process (Prytherch, Sinnott, Howells, Fuller-Love, & O’Gorman, 2012). Despite this, much research on entrepreneurial teams and gender often uses gender as just one of several demographic variables of diversity (e.g., age, education, ethnicity, and functional background). Chowdhury (2005) argues that studies have seldom developed consistent findings. Harrison and Klein (2007) furthermore argue that the framework of diversity is a way of “describing the distribution of differences among the members of a unit with respect to a common attribute” (p. 1200), and that previous mixed results from research on team diversity can be explained by the inability to recognize that the construct of diversity is not only one type of diversity. Instead, it can include three types of diversity:

In studies of entrepreneurial teams, diversity has often been constructed in terms of

In overview articles of women’s entrepreneurship (Achtenhagen & Tillmar, 2013; Ahl, 2006; Hughes, Jennings, Brush, Carter, & Welter, 2012), it is claimed that earlier research has used an individualistic perspective, and neglected contextual and historical factors—for example, the social arrangements in which women are embedded. Ahl (2006) argues that research tends to reinforce the idea that differences between male and female entrepreneurs can be explained at the individual level, rather than at the social or institutional level; thus, we need future studies where women are embedded in collective settings. As noted, our ambition in this article is to contextualize these issues (cf. Welter, 2011).

Scholars have asked for longer longitudinal research designs of entrepreneurial phenomena (Aldrich, 2009; Davidsson, 2008; Martinez et al., 2011; Poole, Van de Ven, Dooley, & Holmes, 2000). The present study uses a longitudinal, long-term approach to capture entrepreneurial processes with several levels of explanations. Thereby, our study also aims at contributing methodological insights. We employ a prospective longitudinal database, covering more than 23,000 Swedish joint-stock company start-ups—specifically, the data consist of complete entry cohorts of ventures founded in 1930, 1942, 1950, 2001, 2003, and 2005. We trace the survival of the ventures in each cohort over a 3-year period, a phase recognized to be the most precarious for survival (Stam & Schutjens, 2006).

Background and Research Framework

In this study, we use the definition of an entrepreneurial team from Schjoedt and Kraus (2009): An entrepreneurial team consists of two or more persons who have an interest, both financial and otherwise, in and a commitment to a venture’s future and success; whose work is interdependent in the pursuit of a common goals and venture success; who are accountable to the entrepreneurial team and for the venture; who are considered to be at the executive level with executive responsibility in the early phases of the venture, including founding and pre-start up; and who are seen as a social entity by themselves and by others. (p. 515)

This definition emphasizes the fact that the entrepreneurial team is a social entity that is recognized both by themselves and by others; that there is a shared commitment and an interdependency in the team; that the members hold a possession of an executive position in the foundation of the venture; and that there is a link between the founders and venture performance.

The literature on organizational performance can essentially be divided into two main views: One view is based on the idea that factors at the individual level—human demographic variables such as human capital, social background, and cognitive ability—can explain performance differences and variations at the organizational level. One clear example is the “traits school” in entrepreneurship (Landström, 2005). This view can be described as “voluntaristic,” as the environment of entrepreneurs has less explanatory power for organizational performance. The other main explanation takes on a “deterministic” standpoint in which conditions that are external to the firm are of greater importance (Mellahi & Wilkinson, 2004; Smith & Cao, 2007). Two subsets of perceptions can be identified within this “deterministic” explanation: One is the

Several explanations for organizational performance maintain that the selection mechanism is effective at several levels; consequently, these are contexts that relate to the individual, to the team, the business, the market, as well as to institutional and macro-levels. Contextualization implies a consideration of situational and temporal boundaries for entrepreneurship. In the present study, phenomena at the

Furthermore, as a team involves social relations, we can analytically conceive the mere presence of an entrepreneurial team in a venture as one particular type of context which differs from the social context of a venture founded, owned, and managed by a solo entrepreneur. The latter must rely on relations to a social network without any venture partner(s). The performance outcomes may therefore vary between the two types of contexts (e.g., Lechler, 2001).

Welter (2011) explicitly distinguishes between omnibus contexts—or contextual “lenses”—and

In accordance with this discussion, our research framework aims at studying the effect of different contexts at different levels. This includes the explicit purpose to measure—or at least the ability to control for—different prevailing contexts when ventures are founded.

Methodological Approach

Following Aldrich (2009), in particular Martinez et al. (2011), our aim was to sample entire initial population of venture start-ups—that is, the mundane, initial population of start-ups. It also includes the objective to measure the survival of those venture start-ups. In several respects, we are able to accomplish this. While we are not able to solve all methodological and theoretical problems—we cannot capture the entire contextual “lens,” nor are we able to investigate the full dynamic relationship between all context dimensions—our research strategy with a prospective cohort approach (Aldrich, 2009; Lippman & Aldrich, 2016) significantly increases the possibility to include and control for several types of contexts at various levels, including chronological time. A cohort is an aggregate of individual units, and differences between cohorts may prevail over both short and long periods (Glenn, 1977). Our empirical data consist of several complete entry cohorts of venture start-ups followed over a predefined period of 3 years—our approach is thus longitudinal and prospective. Ideally, entry cohorts embody

Theory and Hypotheses

Entrepreneurial Founding Teams and New Venture Survival

Already Cole (1959) identified the entrepreneurial team as a central phenomenon in entrepreneurship research, arguing that the social context in which the entrepreneurial functions or activities that initiate and maintain a new venture “proceeds in relationship to the situation internal to the unit itself, the social group that really constitutes the unit, and to the economic, political, and social circumstances—institutions, practices, and ideas which surround the unit” (p. 8). Later, Gartner (1989) emphasized the collective perspective, underlining the need to move away from the single-entrepreneur perspective. Since then, the interest in venture teams as analytical units has increased. Attempts to capture the venture team as a social phenomenon in the 1980s and 1990s resulted in several interesting results. Survey articles indicate that ventures founded by teams perform better than those started by single founders: In their overview, Cooper and Gimeno-Gascon (1992) reported that in four of five studies, ventures started by teams performed better than those started by single founders. Furthermore, Storey (1998) found seven studies that tested the hypothesis that ventures started by more than one founder are more likely to grow than those started by a single person. Five studies indicated support for this hypothesis. Organizational survival is generally a less employed independent variable in studies of entrepreneurial teams: In their review, Zhou and Rosini (2015) found that in the operationalization of venture performance, growth was the most common variable. In a review of a dozen empirical studies, Lechler (2001) found that 10 studies indicated a significant positive relation between the existence of an entrepreneurial team and venture growth, while no clear results were found in the two studies that used survival as the dependent variable; for instance, Cooper, Gimeno-Gascon, and Woo (1994) found that ventures with more than one founder were more likely to grow but not to survive.

More recently, Stam and Schutjens (2006), investigating a large sample of ventures in a one-cohort longitudinal study, show that a higher proportion of solo start-ups were terminated within a 6-year period as compared with ventures started by a team. Similarly, in a large-sample, multisector study by Gueguen (2013), the survival rate for ventures started by entrepreneurial teams is significantly higher over a shorter period (3 years), but this difference does not hold over longer periods. Recently, highlighting the complex relationship between solo-start-ups, start-up teams, gender, and business failure, Yang and del Carmen Triana (2017) study a representative sample of a little more than 10,000 U.S. start-ups, followed longitudinally over a 6-year period. There was no significant difference in failure between businesses started by solo-entrepreneurs and those started by teams in general. Furthermore, nonspousal same-sex teams—that is, teams consisting of either all-male or all-female teams—did not reveal any difference in performance as compared with mixed-gender teams or (as noted above) solo-start-ups.

Past results are therefore not entirely decisive regarding the effect of teams or founding teams (or the [gender] composition of teams). Several researchers have emphasized that team ventures should not be seen as an unproblematic concept, one reason being the problem of holding an entrepreneurial team together (Eisenhardt & Schoonhoven, 1990; Lechler, 2001). Diversity in groups is often regarded as a “double-edged sword”—Milliken and Martins (1996, p. 403) and Birley and Stockley (2000, p. 296) used the same metaphor when discussing entrepreneurial teams and venture performance. The start-up process in a venture contains risks, uncertainties, and ambiguities (Sarasvathy, 2001), and it is proposed that entrepreneurial teams are a social favorable context to parallel manage risks, uncertainties, and sense making by seizing, exploring, and exploiting venture opportunities (Larsson Segerlind, 2009). Therefore, on one hand, the team can enable innovative development and fast growth; on the other hand, it can be a source of conflict and instability which may lead to the dissolution of the venture (Hambrick, Cho, & Chen, 1996; Kanter, 1983; Khan, Breitenecker, & Schwarz, 2014). Thus, even if past research on the relationship between venture survival and entrepreneurial teams is inconclusive, we formulate the following first hypothesis:

Entrepreneurial Founding Team Composition, Gender, and New Venture Survival

The first attempts to explain both the formation and (assumed) performance superiority of teams were based on the assumption that a higher degree of variety of resources and capabilities in the team could explain their success (Kamm & Nurick, 1993; Sandberg, 1992). However, in empirical findings, heterogeneity showed no direct significant impact on venture performance (Lechler, 2001). Since the early 2000s, scholars have tried to develop more valid concepts and models. Forbes, Borchert, Zellmer-Bruhn, and Sapienza (2006) found two ways of classifying the literature. Team formation is either a resource-seeking behavior or a manifestation of interpersonal attraction, where trust and relationships are already established. The latter perspective is more related to diversity in terms of

The focus on the contextual aspects of entrepreneurial teams makes the theoretical assumptions visible in earlier research about diversity in entrepreneurial teams: Especially Harrison and Klein’s (2007) framework on different constructs of diversity may clarify past shortcomings and mixed results in earlier studies. They do not only argue that diversity is often constructed in terms of variety, separation, or/and disparity, but each of these constructs also brings different theoretical assumptions. Diversity in types of variety can be said to represent the resource-based theoretical perspective; the diversity-type separation is more related to social similarity attraction theory. The “missing link” in entrepreneurial team research is the use of diversity in terms of disparity. Diversity in type of disparity is rather connected to more traditional sociological theories in terms of social power, inequality, status, privileges, and so on (Ragins & Sundstrom, 1989). Power is here defined as “influence by one person over others, stemming from a position in an organization, from interpersonal relationships, or from individual characteristics” (p. 51), and can be categorized as objective or perceived. Disparity as a diversity construct is rare in empirical research on entrepreneurial teams as well as in theoretical interpretations of outcomes. However, there are exceptions (Hellerstedt, 2009; Yang & Aldrich, 2014; Yang & del Carmen Triana, 2017); for instance, Hellerstedt (2009) found that disparity (vertical diversity) in terms of differences in status was a promising theoretical perspective as it could explain much of her findings related to new venture team dynamics. Yang and Aldrich (2014) also found vertical diversity in terms of differences in gender stereotypes as a strong mechanism for explaining gender inequalities and the constraining of women’s access to power positions in the entrepreneurial team.

Zhou and Rosini (2015) argue that due to a limited number of studies and inconsistent results—and the use of different performance measurements—no conclusions can be drawn regarding the effect of entrepreneurial team diversity. Additional reasons for inconsistent findings in the past research may be improper measurements of team diversity (Harrison & Klein, 2007). However, scant empirical research supports the notion of a positive link between gender homophily, especially male homophily, and venture survival 1 year after the start (Ruef, 2010). Therefore, and before we develop hypotheses specifically related to gender and the gender composition of founding teams, we first hypothesize on how team gender diversity and homogeneity affect new venture survival. Defining team homogeneity as ventures founded by either all-male entrepreneurial teams or all-female teams, we formulate the following hypothesis:

Women’s entrepreneurship has been a well-established research agenda since the 1990s. The biological sex of entrepreneurs, and the analytical distinction between biological sex and gender (i.e., the social construction of sex), have therefore become a commonly included variable; stronger linkages between female entrepreneurship and gender theory are evident in recent research (Holmquist & Carter, 2009). A central discussion of female entrepreneurship concerns whether women are systematically discriminated, suggesting that ventures owned and/or managed by women exhibit a poorer performance relative to those owned by males. A “gender gap”—explained by systematic or structural factors in society—has been acknowledged to deprive women of vital resources such as education, networks, and capital (Anna, Chandler, Jansen, & Mero, 2000; Watson, 2002). Past research has shown that women entrepreneurs in the start-up stage or in the growth phase have less access to financing and venture capital (Gatewood, Brush, Carter, Greene, & Hart, 2009; Marlow & Patton, 2005). For that reason, businesses owned by women underperform by displaying smaller growth and smaller profits as well as smaller survival chances. However, Klapper and Parker’s (2011) review of the extant literature finds that while there are significant differences in performance between male- and female-owned firms, past empirical research does not systematically indicate the existence of a gender gap. In essence, two major schools of thought exist in this research:

The above discussion can generate disagreeing assumptions on the particular effects of gender and gender homogeneity on venture performance when using empirical data that are both historical and modern. It can be recalled that Hypothesis 2 states that gender homophily will increase the likelihood of venture survival. Consequently, mixed-gender team ventures will have lower survival probabilities. Past empirical results have nonetheless found that male homophily in particular has a stronger impact on future venture performance (Ruef, 2010). Even if Yang and del Carmen Triana (2017) were not able to separate all-male and all-female teams, they found that female entrepreneurs’ businesses are more likely to fail as compared with male entrepreneurs. Therefore, we formulate the following two related hypotheses on gender similarity:

Institutional Transformation, Gender, and New Venture Survival

The final aim of our study was to investigate whether the likelihood of survival for female-founded ventures—solo entrepreneurs and teams—has changed over time. Until now, we have in our framework focused on the social contexts, but as Welter (2011) claims, the “contextual lens” turns the attention toward multiple context dimensions and how they are connected. As all institutions, gender relationships are structured according to both formal and informal rules, or institutions (North, 1990; Rosenberg & Birdzell, 1986; Welter, 2011). Therefore, institutions structure human exchange, and both formal and informal institutions are subject to change over time, especially in the long term. Formal institutions, such as constitutions and laws, are complementary to informal institutions, and sometimes they even supplant informal institutions to increase efficiency, defining the behavioral constraints of economic agents such as entrepreneurs. During uncertainty, the function of formal institutions is to facilitate exchange. Informal institutions are derived from culture, regulating societal behaviors; cultural traits have a tendency to survive over time, often longer than formal institutions; and North (1990) maintains that the combination of formal and informal rules defines the institution. This combination provides the basis for persistent incremental institutional change in the game between agents and interests competing for economic, social, and political power.

Changes in formal and informal institutions are seldom synchronized; a formal institutional change may not always alter the informal institution and social norms, at least not in the short term. That is also why informal structures and social relationships, such as discrimination, may endure over long periods of time. The implications of institutions on entrepreneurship in general (Baumol, 1996), on entrepreneurial entry and entrepreneurial intentions (e.g., Stenholm, Acs, & Wuebker, 2013), as well as on female entrepreneurship (e.g., Estrin & Mickiewicz, 2011) are today significant research and policy agendas. It is often concluded that institutional arrangements affect entrepreneurial outcomes and intentions, such as entry into self-employment.

Much research is regularly cross sectional, and institutional change over longer periods is therefore often difficult to include in the analysis (Aldrich, 2009; Martinez et al., 2011; Welter, 2011). However, we may think of institutions as either favorable or unfavorable contexts, or conditions that will affect particular economic actors or groups, and these contexts are subjected to change over time (Rosenberg & Birdzell, 1986). As in several other developed economies, the institutional context for women entrepreneurs in Sweden and for women as a social group has changed profoundly during the last 100 years (Bladh, 1997). Significant economic reforms in the 1860s gave men and women formal equal rights to run a business, but this did only pertain to unmarried women. An unmarried woman had no majority but she had the right to apply for majority at court (her right was the right to apply), otherwise her father would be her legal guardian. If a woman with majority married, she once again received a legal guardian: the husband. If widowed, a woman received majority. Women formally received equal rights in 1921, but they were still subjected to several informal and structural constraints in numerous ways (Axelsson, 2006). Both informal and formal institutional conditions, such as restricted rights to control personal assets, remained for women well into the early 1950s: Bersbo’s (2012) study of Swedish women’s economic independence and women’s struggle for gender equality shows that informal institutions, and a discourse which deprived women of equal economic rights, remained during a large part of the 20th century. Above all, Bersbo shows that the progression toward women’s economic rights was an extended and gradual process: political and economic reforms in the early 1920s, the late 1930s, and in the early 1970s gradually improved the formal conditions for women economically (see also Sundin, 1995; Svanström, 2003). It is not until the 1980s, in particular the 1990s, that we can observe a more distinct change in both informal and formal institutions for female entrepreneurship. New types of women’s social movements, focusing on female entrepreneurship, saw the light of the day, and economic policy has distinctly acknowledged and actively supported women entrepreneurs in Sweden in a few recent decades (Wottle & Blomberg, 2011).

Following these insights and the suggestions from Yang and Aldrich (2014), we make the assumption that the institutional context affects the social context for women entrepreneurs in the sense that an institutionalized gendered logic, based on unequal gender stereotypes, may still be a hidden structure and a power mechanism that constrains women entrepreneurs. Time is a contextual factor; the formal and informal societal conditions for women entrepreneurs have most likely improved over the course of time. Thus, and conditional on the previous hypothesis (H3), we formulate the following hypothesis:

Method and Data

As noted in passing, the methodological approach in this study is to use complete entry cohorts of ventures, founded during different periods. Our data consist of six individual birth cohorts of Swedish joint-stock companies, founded in 1930, 1942, 1950, 2001, 2003, and 2005. 3 The dataset covers a total of 22,974 joint-stock company start-ups, and records new venture survival in each cohort over a 3-year period. With the aim of producing a long dataset that is as homogeneous as possible, we have combined very different source materials, and we utilize two subsets of data. One subset—consisting of the cohorts from 1930, 1942, and 1950—is constructed from unprinted, archival public sources (Swedish Patents and Registrations Office, preserved at the Swedish National Archives). 4 During the assembly of this particular subset, information on the company founders pertaining to team size and to gender was recorded. The second subset—the cohorts from 2001, 2003, and 2005—consists of data commonly not readily available in public databases. It has been made available exclusively to us by the Swedish Agency for Growth Policy Analysis. 5

As noted, our aim was to create a homogeneous database in the sense that independent variables in the study should not differ or be biased, neither within nor between different birth cohorts. Specifically, indicators for firm survival, gender, line of business, and corporate form should be consistently defined. This is not an uncomplicated task, considering that very different sources have been utilized. Our dataset is not flawless: To begin with, and as we only have two observation points in time for each cohort, we are not able to study whether a venture experiences succession during the 3 years of observation. Thus, we measure how certain characteristics of the ventures upon founding—team, team composition, and gender—would affect venture survival (Carroll & Khessina, 2005; Ruef, 2010). Furthermore, our dataset excludes other corporate forms such as trading firms or sole proprietorships. To be able to make valid comparisons, we have chosen this type of corporate form, and the reason is that the three cohorts from 1930, 1942, and 1950 concern joint-stock companies only. Historical cohorts on other corporate forms are virtually impossible to collect as no archives have been systematically preserved. Furthermore, the older subset consists of companies founded in the capital of Stockholm as it takes considerable time to create a birth cohort of companies from preserved public records archives. The subset of firms founded in 2001, 2003, and 2005 covers the entire country, and therefore it covers substantially more companies. However, the 1930-1950 dataset includes a rather large share of the total number of joint-stock companies entering in these years—for example, Cohort 1930 covers approximately 22% of all newly founded joint-stock companies in Sweden that year (Statistics Sweden, 1940, 1951). At present, we are not able to evaluate whether companies founded in Stockholm differ from those founded in the rest of the country.

Another factor for which we are presently unable to control is the start-up size of the ventures, as we lack suitable indicators; we acknowledge that there is ample support for the notion that business performance and survival are positively correlated with both firm age and firm size (e.g., Hart, 2000). In addition, while the older subset (1930-1950) measures entry and survival at the level of the firm, the other subset measures survival at an aggregated level—specifically, it records

Our data are analyzed with binary logistic regression using frequency weights: The data have been arranged such that we have one observation per response category at the start, t0, and one observation after 3 years, at t3, for that particular response category. Survival over 3 years is the dependent variable, and it is a binary outcome (0/1)—consequently, for each response category, we measure the survival frequency between t0 and t3. Overall, the different variants of categories give 120 rows of observations for the total of 22,974 ventures. It is acknowledged that the relative imbalance in sample sizes between the cohorts founded 1930-1950 and 2001-2005, respectively, may influence our results.

Variables

As noted in passing, the

Both entrepreneurial founding teams and solo founders, as well as the

To test the hypothesis on

We also use

It is acknowledged that possible disadvantages with our empirical data lie in an inability to precisely measure and/or control for several factors. Furthermore, there is an imbalance in the size of the two main datasets (1930-1950; 2001-2005) which may influence the analysis. However, the explorative approach of our study and the prospective longitudinal design of our empirical database have the potential to generate new knowledge and new research questions.

Results

We present descriptive statistics for survival rates, teams, and gender composition in seven cohorts in Table 1, not only the six cohorts that are included in the statistical analysis. First, it can be noted that the survival rate over 3 years differed substantially between cohorts: Around 67% of the ventures survived for 3 years or more in the cohort from 1930, while the highest 3-year survival rate is found among firms in the cohorts from 1942 to 1950 (above 90%). In the cohorts from the 2000s, Cohort 2005 has the highest survival rate, which is nearly 86%. Overall, a little less than 80% of the ventures in the entire dataset survived for 3 years. The variation in survival between cohorts has no simple, straightforward explanation. However, the first years for the ventures in Cohorts 1912 and 1930 coincide with worsening macroeconomic conditions—in the case of Cohort 1912, the outbreak of World War I in 1914; in the case of Cohort 1930, the economic depression in the early 1930s. Furthermore, ventures in Cohorts 1942 and 1950 were founded during a period of economic growth and economic protection; in particular, during World War II, the Swedish economy was strongly regulated, and it expanded significantly. Similarly, in the early 2000s, Swedish economic growth fell significantly; between 2000 and 2001, it was less than 1% and merely 1.8% in 2002 (Schön & Krantz, 2015). The economy gradually recovered, and it is likely that the increasing 3-year survival rates in Cohorts 2001, 2003, and 2005 partially reflect this process. Overall, these very different survival rates between the entry cohorts clearly reveal the advantages of a multicohort study. If we are not able to control for the (historical) period of entry, and the fact that one set of ventures may have systematic and structural differences in survival as compared with other sets of ventures, we may run the risk of confusing the factors that affect venture performance.

Overall, the social structure of our data (Table 1) resembles other datasets on solo and team ventures (cf. Yang & del Carmen Triana, 2017), particularly concerning our own cohorts from the 2000s. For instance, nearly half of the new businesses were started by teams, and there is an overall dominance of males (which diminishes over time). Furthermore, the descriptive statistics preliminary suggests that ventures founded by females (single founders as well as teams) have a lower survival rate as compared with those founded by males. Around 54% of the ventures were started by a single founder, whereas some 46% were started by a team. We also observe variation across time. No venture in Cohort 1912 was started solely by women—neither as solo-start-ups nor in teams—and a smaller share of women than men was involved in mixed-gender teams. The figure is also relatively low for the Cohorts 1930, 1942, and 1950, in both absolute and relative terms. In this particular dataset, it became less common to found a venture with a team (falling from around 90% in the early 1900s to around 40% in the early 2000s). Similarly, mixed-gender founding teams were somewhat more common during the first half of the 20th century as compared with the early 21st century. Without doubt, the share of females engaged in new venture creation (either as single founders or in teams) seems to have increased over time; this is also supported by other data (Statistics Sweden, various years). However, as can be observed, the majority of ventures are founded by males. There is also a variation across different categories of ventures. Specifically, the overall 3-year survival rate of ventures started by entrepreneurial teams is higher (81.1%) than those founded as solo start-ups (77.9%). For solo venture start-ups, male founders have higher survival rates than female founders; the difference is nearly 5 percentage points. Similarly, ventures founded by all male teams reveal a higher survival rate than ventures founded by all females in our data—nearly 82% against 78.5%. Mixed-gender founding teams position themselves in between (79.9%).

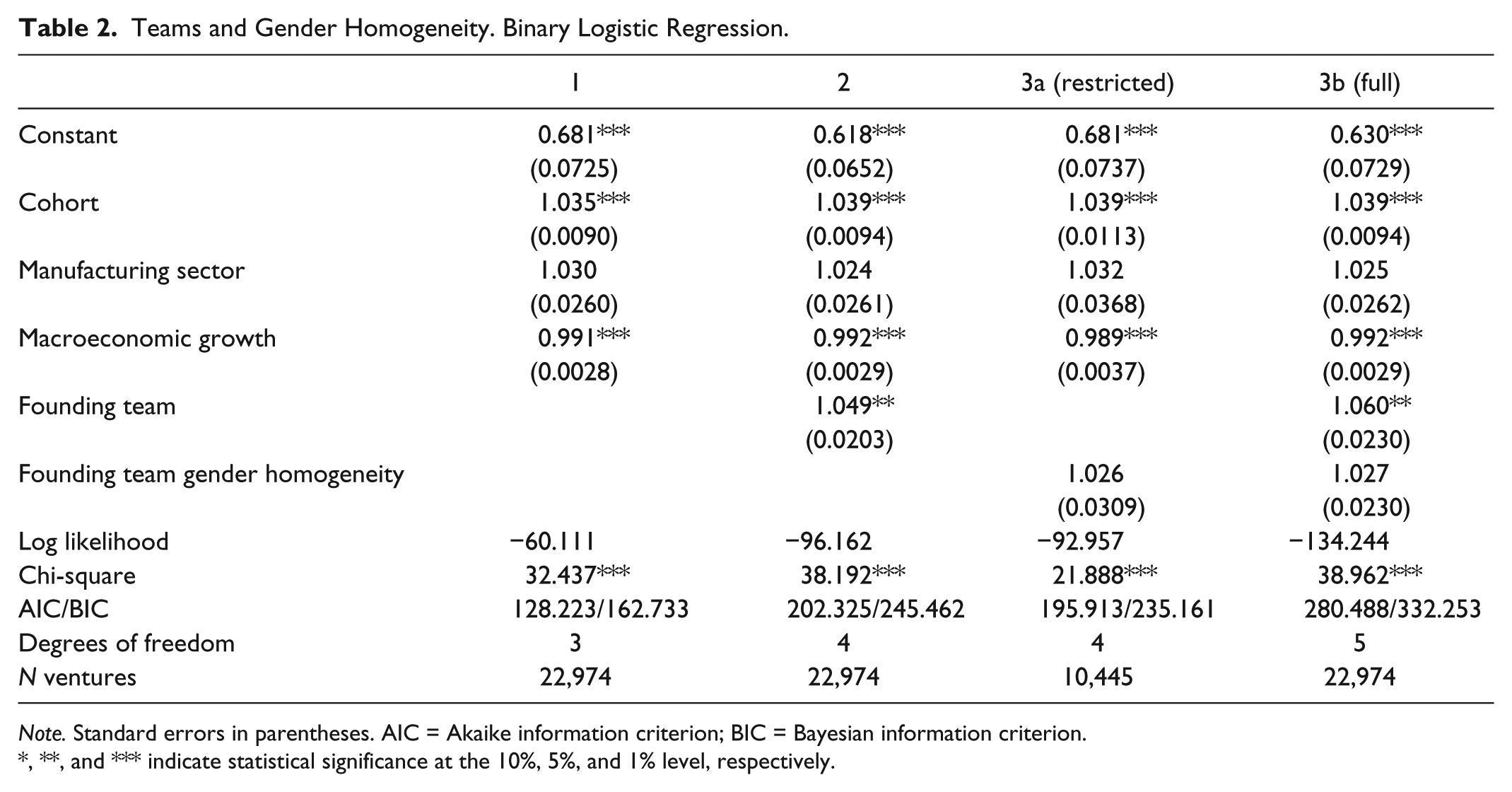

We ask in our study if differences in venture survival can be explained by team gender composition, gender, and institutional change, analyzing the data with binary logistic regression. The first results are presented in Table 2. Coefficients are reported as odds ratios: If a coefficient exceeds 1.0, the effect of an independent variable increases the probability of survival; if less than 1.0, the probability decreases. Model 1 is the baseline model, controlling for cohort, sector (service/trade and manufacturing), and macroenvironmental conditions at the time of founding and during the first 2 years of each cohort (GDP growth). Model 2 introduces a variable for ventures started by founding teams. As can be observed, and when controlling for cohort, sector, and macroconditions, the presence of teams in a venture significantly increases the probability of survival. This result supports Hypothesis 1: Founding teams will increase the likelihood to survive.

Teams and Gender Homogeneity. Binary Logistic Regression.

, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

Hypothesis 2 proposed that gender homogeneity increases the likelihood of survival. Model 3 aims at testing this hypothesis, and the model comes in two variants that both introduce the variable for ventures founded by homogeneous teams (either all male or all female). Model 3a is a “restricted” model and only analyzes ventures founded by teams—solo start-ups are here excluded from the analysis. The model shows that it cannot be established that team gender homogeneity per se increased the survival prospects in comparison with teams consisting of both males and females. Similarly, Model 3b, using the entire sample (also including solo start-ups), gives no support for the assumption that founding team homogeneity increases the survival performance. Even if the odds ratio is greater than 1.0, it is not significant in either variant of Model 3. Therefore, the second hypothesis (H2) receives no support.

Table 3 presents results with the aim of testing the third hypothesis (H3), which stated that male gender homogeneity in a founding team will lead to a higher probability of survival as compared with other team compositions (H3a), and that solo start-ups by males will have a higher probability of survival (H3b). The results in Table 3 give partial support for the notion that all-male founding teams perform better than other team compositions. Specifically, they perform better than all-female-founded ventures (however, no significant difference is found between all-male and mixed-gender founder teams). Like Model 3, Model 4 comes in two variants: one restricted version that excludes all solo start-ups, and the other full version that includes all solo start-ups. Model 4a, which only focuses on ventures founded by teams, shows no significant difference in survival between mixed-gender founding teams and all-male founding teams, even if the odds ratio is less than 1.0. Similarly, ventures founded by all-female teams exhibit no significant difference in survival as compared with all-male founding teams. Hypothesis 3a thus receives no support. However, when using solo start-ups as a control variable (having a significantly lower survival rate than ventures founded by teams; cf. Models 2 and 3a), the full-sample analysis (Model 4b) shows that all-female founding teams had a significantly lower probability of survival as compared with ventures founded by all-male teams (significant at the 10% level; level of significance = .08). Thus, given that we include

Gender Composition of Teams and Solo Start-Ups. Binary Logistic Regression.

, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

However, these results are not entirely conclusive, as there may well be no substantial difference(s) between different team constellations. Specifically, it is highly probable that solo start-ups are, in fact, responsible for the obtained (and rather low) significant effect for female-team-founded ventures in Model 4b: When including only solo-founded ventures is an alternative model (not reported here) and using solo-ventures founded by males as the reference category, it turns out that male-founded ventures have a statistically higher probability (close to the 5% level: significance = .06; odds ratio = 1.074) of surviving with their business as compared with solo ventures founded by females. In fact, this result mirrors the obtained result on solo-founded ventures by females in Model 5a (reported below). Hence, we can here only conclude that the assumption of female founding teams being less (or more) prone to survive as compared with other constellations—males or mixed-gender teams—receives scant support. Nonetheless, these results also indicate that analyses of samples only consisting of team-founded ventures (such as in Model 4a), and that do not control for other types of firms that enter or exist during the same interval (here: solo start-ups), may produce different and potentially skewed results.

Model 5 aims at testing Hypothesis H3b: Model 5a is restricted and only includes solo start-ups; here, the variable for ventures of single female founders shows a significantly lower survival probability (also supported by the alternative model discussed above). When including the full sample (5b), thus also including ventures started by teams, this negative effect remains—ventures started by single female founders showed a lower probability of survival. Overall, from Models 4 and 5, we can only conclude that ventures founded by single female entrepreneurs had a higher risk of exit within 3 years from the start; any gender-specific homogeneity effect—for both male and female teams—is difficult to discern.

Table 4, finally, reports the results that test the fourth hypothesis (H4), which stated that improvements in the institutional and societal context for female entrepreneurs decrease the gender differences in the probability of new venture survival. It can be recalled that we hypothesized that there was a positive increase in the overall institutional conditions for women entrepreneurs during the century. In preliminary tests, we constructed separate models for ventures founded by all-female entrepreneurial teams and for solo start-ups founded by female entrepreneurs, respectively. No significant results were obtained; furthermore, the number of observations on female solo-entrepreneurs in the older cohorts is very few. We therefore test the final hypothesis (H4) by including indicators of all types of female-founded ventures, irrespective of whether they are founded by teams or are founded as solo start-ups.

Gender and Institutional Conditions. Binary Logistic Regression.

, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

Table 4 presents two models. As can be observed, Model 6 comes in two variants: 6a and 6b. As in our previous tests, Model 6 is quite “invariant” to time—rather, we treat all our observations as a single “cross-section.” To assess whether it can be established that female-founded ventures are generally less prone to survive, we contrast the survival of male-founded ventures (both solo ventures and team ventures) and mixed-gender ventures against ventures founded by females (solo start-ups and team start-ups) in the cohorts from 2001, 2003, and 2005 in Model 6a (thus excluding the cohorts from 1930, 1942, and 1950). The results show a significantly lower survival rate for Swedish ventures started by females in the early 2000s (however only at the 10% level). As we assume ex ante that the conditions for female entrepreneurs have improved over time in Hypothesis H4, it is not surprising that this pattern remains in the full model, Model 6b. Here, female-founded ventures generally exhibit lower survival rates across time as compared with ventures founded by males (solo or in teams) and mixed-gender teams. In particular, the full-sample analysis in Model 6b (Cohorts 1930-2005) gives statistical support for this conclusion: Both male-founded ventures and mixed-gender team-founded ventures have a statistically higher probability of surviving. Thus, once more, we find support for the assumption that female-founded ventures had a lower propensity to survive (see Hypothesis H3).

However, Model 7 attempts to analyze differences between different periods. This model introduces interaction terms for institutional conditions for both male founding entrepreneurs (solo as well as teams) and mixed-team founding entrepreneurs in which we contrast the period 2001-2005 (1) against the previous period, 1930-1950 (0). The odds ratios for both interaction terms are smaller than 1.0 and significant. Our hypothesis receives support: in this model, the relatively better performance by ventures founded by men and mixed teams weakens over time, relative to ventures founded by females (solo as well as teams). This suggests that ventures founded by women in the 2000s may have better survival chances in comparison with ventures founded by women under more disadvantageous institutional conditions. 7 In conclusion, we find that some, but not all, of our hypotheses receive support in our analysis and in our dataset.

Discussion and Conclusion

In this study, we initially asked if there is a difference in the likelihood of survival for ventures founded by an entrepreneurial team, as compared with ventures founded as solo start-ups. When controlling for initial conditions—cohort, sector, and macroenvironmental conditions—our empirical results showed that ventures with an entrepreneurial founding team had a significantly increased survival probability. Earlier convincing studies have found that entrepreneurial teams perform better than single entrepreneurs, measuring performance in terms of venture growth. When it comes to performance in terms of

In explaining the higher survival rate for entrepreneurial founding teams, we argue that the start-up process in a venture contains risks, uncertainties, and ambiguities (Sarasvathy, 2001); under these conditions, it can be assumed that the social context of stakeholders, in terms of an entrepreneurial team, is a favorable contextual setting (cf. Larsson Segerlind, 2009).

The second research question asked whether the probability of venture survival is affected by the gender composition of founding teams. Earlier studies are scarce and they have produced mixed results (Zhou & Rosini, 2015), but they indicate that gender-homogeneous teams have better survival rates than heterogeneous teams (Ruef, 2010). However, we did not find such an effect. It has been argued that diversity, in terms of separation (homogeneity), is a positive factor for explaining not only the formation but also the performance of ventures. However, our results indicate that homogeneity is not a strong explanatory factor for performance in terms of survival. Our findings are in line with recent results (Yang & del Carmen Triana, 2017), questioning earlier models that claim an advantage from team homogeneity. Another explanation for our results can be that our samples of heterogeneous teams most likely include both spouse- and nonspouse teams. It is often argued that mediating factors such as trust and mutual commitment (e.g., in spouse teams) make the entrepreneurial team capable of handling a high degree of risk, uncertainty, and sense making in early phases of the venture. Previous results have shown that spouse teams have better survival rates than both nonspouse teams and homogeneous teams (Hellerstedt, 2009; Ruef, 2010). Presently, we are unable to distinguish these categories of teams.

When we went further, examining the effect of different gender compositions, the results were mixed. The assumption of a lower survival probability for all-female teams only received weak support. Furthermore, we found no support for a difference in survival for mixed-gender teams, as compared with all-male teams. These results indicate a gender effect on venture survival; however, the variable for single female founders exhibited a significantly lower survival rate. A bold conjunction of this observed lower survival rate for single female founders is that unfavorable institutional conditions affect the chances of survival of this type of ventures. In line with earlier studies (Lechler, 2001; Yang & del Carmen Triana, 2017), we interpret these partial and mixed results as an overall gender effect (more than a demographic initial condition as in much past research). These results may suggest that research needs to comprehensively include social power as a theoretical perspective. The role of and the distribution and possession of power, status, prestige, and the attitudes to gender stereotypes—both in the internal social setting of the ventures and in relation to the external society—need to be further elaborated on. Furthermore, the empirical results related to the third hypothesis in the present article, that ventures founded by males will have a higher likelihood to survive, support these statements.

As gender is an integral phenomenon in our study, we asked in our third and last research question if venture survival in general is conditional on founders’ gender, and whether this relationship has changed over time. In line with past results, we found that female-founded ventures had a higher likelihood to exit relative to other constellations (cf. Yang & del Carmen Triana, 2017). We further assumed that gender differences in the likelihood of new venture survival will decrease if the institutional context for female entrepreneurship becomes more favorable over time. We found distinct, significant support for this hypothesis. Our interpretation of the results is that the mix of unfavorable formal and informal institutions of that time and age could partially explain the lower survival rate for female founding entrepreneurs in the first half of the 20th century. At the beginning of the 21st century, most of the unequal formal institutions have disappeared, and there has also been a progress of more favorable

If we conclude the empirical results and our empirical contribution, we find that initial contextual social conditions, in terms of a venture founded by an entrepreneurial founding team, have an effect on new venture survival (over 3 years). As noted, these results are partly at odds with recent research (Yang & del Carmen Triana, 2017). However, Yang and Triana also question earlier models on the advantage of team homogeneity, which we have also found in our study. Furthermore, their results show that female ventures underperform relative to male-founded ventures, and we have discovered a similar pattern for Sweden—historically, but also presently. We also find that gender effects on new venture performance may interact with changes in the institutional environment. In that sense, time is an important and essential contextual factor in explaining entrepreneurial phenomena, also when it comes to entrepreneurial teams. As for the theoretical conclusions and contributions of the article, we argue that Harrison and Klein’s (2007) conceptual and theoretical clarification of the three constructs of diversity—

Implications and Future Directions

A rising awareness of time and context (Welter, 2011)—and of time