Abstract

Keywords

Introduction

Observing the trend and forecasting the future are always required in all kinds of market. In understanding Big Data, people are more interested to obtain the trend and dynamics of a given set of temporal data, which in turn can be used to predict possible futures.

Classic statistical methods are usually used to perform the task, such as regression analysis, cluster analysis, and so on. As a branch of statistics, time series analysis (TSA) is very popular for modeling temporal data. 1 Great efforts have been put in the application of TSA in the temporal market analysis. In 1970, Box and Jenkins proposed the autoregressive integrated moving average (ARIMA) model. 2 In order to handle time-varying property of variance, Engle derived autoregressive conditional heteroscedasticity (ARCH) model. 3 Next, Bollerslev (1986), Glosten et al. (1991), and Nelson (1991) derived generalized ARCH (GARCH) model, threshold ARCH (TARCH) model, and exponential ARCH (EARCH) model, respectively.

One of the disadvantages of these statistical methods is that large amount of market data is required. In such cases, numerical methods, i.e. ordinary differential equations (ODE), 4 partial differential equations (PDE), or stochastic differential equations (SDE), would be taken into account.

This paper examines a modified ODE approach and compares it with TSA in modeling the price movements of petroleum price and of three different bank stock prices over a time frame of three years. The market data were obtained from the official web page. 5 Computational tests consist of a range of data fitting models in order to understand the advantages and disadvantages of these two approaches. Then, a modified ODE model, with different forms of polynomials and periodic functions, is proposed. Numerical tests demonstrate the advantages of such modification. Computational properties of the modified ODE are studied.

The rest of this article is organized as follows. In the upcoming section, ARIMA model and an ODE method are introduced and then results of them are compared. Subsequently, the modification of the ODE model is presented and the empirical analysis is shown. Finally, the article is concluded in the last section.

The ARIMA and the existing ODE models

Fundamental methods

Time series analysis comprises methods for analyzing temporal data. Models for time series data contain many forms representing different stochastic processes. In statistics and econometrics, and in particular in TSA, the autoregressive integrated moving average (ARIMA) models are often applied in some cases where data show evidence of nonstationary. Wan and Wen 6 found that ARCH model did not always show better compared to ARIMA model. For simplicity, attention was only given to ARIMA model in this section.

ARIMA models are generally denoted by ARIMA

Given the time series of data

And the symbol

Case

Next, considering the Cauchy initial value problem

One can solve equation (2) by means of numerical integration or obtain an analytic solution if

One approach for solving equation (2) is given by Lascsáková.

8

The particular solution of problem (2) is

Substituting the point

From equation (3),

At the next time

From equation (5),

Generalizing the previous principle, one can get the solution of problem (2) in the following form

Here,

Comparison of the TSA and the existing ODE model

This section compares the time-domain TSA method given in equation (1) and the ODE approach given in equation (2) in modeling the price movements of petroleum price and of two bank stock prices over a time frame of three years.

For the observed data

Let

For petroleum data in 2013, an appropriate model is ARIMA(0, 1, 13)

The calculated results are shown in Table 1. The table indicates that all the APEs of TSA are less than 5%. There are 249 APEs of ODE and only one APE of ODE is not less than 5% but less than 7.5%. It seems that there is almost no difference between these two approaches in this sense. But, the MAPE of TSA is less than that of ODE. It is well known that APE and MAPE are the smaller the better. As a consequence, the TSA method is preferred in the market.

Comparing ODE and TSA of petroleum price (2013).

APE: absolute percentage error; ODE: ordinary differential equation; TSA: time series analysis.

For petroleum data in 2014, an appropriate model is ARIMA(6, 1, 0)

For petroleum data in 2015, an appropriate model is ARIMA(1, 1, 0)

The results of comparing ODE and TSA of petroleum price (2014, 2015) are shown in Tables 2 and 3.

Comparing ODE and TSA of petroleum price (2014).

APE: absolute percentage error; ODE: ordinary differential equation; TSA: time series analysis.

Comparing ODE and TSA of petroleum price (2015).

APE: absolute percentage error; ODE: ordinary differential equation; TSA: time series analysis.

Similarly, this paper also worked on the share values of two banks over a period of about 750 days. The results are obtained in Table 4.

Comparing ODE and TSA of bank share values.

APE: absolute percentage error; ODE: ordinary differential equation; TSA: time series analysis.

From the above examples, TSA seems to show better results compared to ODE. However, it is possible to modify the form of the derivative given in equation (2).

Modification of the ODE model

There are different ways of modifying the ODE model given in equation (2). For example, the form of the derivative given in equation (2) may be changed. This section introduces several alternatives in such modification.

If the data

Several different forms of

Possible forms of

Problems (9) and (10) are actually separable differential equations. A general form, which leads to a nonseparable differential equation, is given as below

It should be noted that

The unknown parameters

The bigger the values of

Empirical analysis

Applying the above ODEs (9), (10), (11), and (12) to the petroleum data and three bank share prices, some improved results are obtained. In practice, one would prefer equation (12), which consists of a polynomial and a periodic function. The results are shown in Tables 6 to 11.

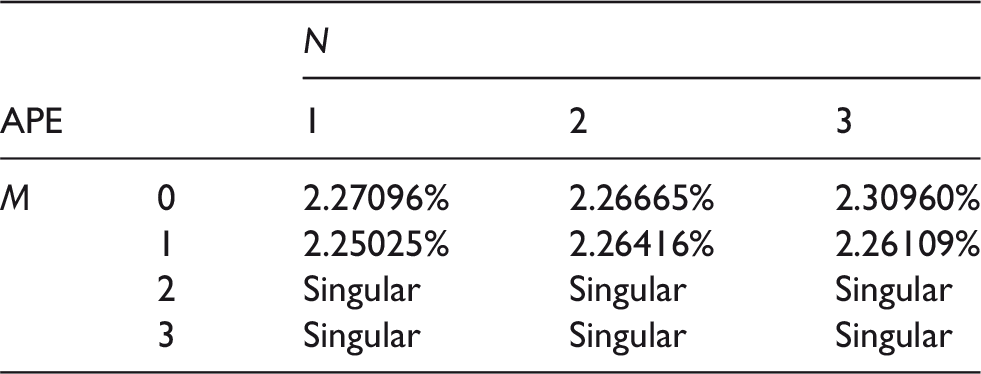

MAPE of petroleum (2013) according to equation (12).

MAPE: mean absolute percentage error.

MAPE of petroleum (2014) according to equation (12).

MAPE: mean absolute percentage error.

MAPE of petroleum (2015) according to equation (12).

APE: absolute percentage error.

MAPE of Barclays bank according to equation (12).

APE: absolute percentage error.

MAPE of Lloyds bank according to equation (12).

APE: absolute percentage error.

MAPE of RBS bank according to equation (12).

APE: absolute percentage error.

In the aforementioned tables, one could choose the best model with the smallest MAPE. For example, for petroleum data in 2013, the smallest MAPE occurs when

The estimated parameters.

The results of equations (2) and (12) can be compared. As can be seen in Table 13 the modified ODE given in equation (12) does improve the results with regard to MAPE.

MAPE compared with different

Conclusions

In order to obtain the trend and forecast the future with higher accuracy, the idea of modifying the ODE model is proposed and the form as in equation (12) seems to be the best modification. Based on the obtained result, it can be stated that such modification provides good understanding of the trend and the dynamics of the price movement. This provides a good way forward in forecasting. Furthermore, on comparison with the statistical methods, numerical methods for ODEs show that fewer historical market data are required.

Finally, recalling the following problem, which involves a deterministic function

This paper provides an insight on various forms of the right-hand side of problem (13). The authors anticipate that this work will lead to a systematic and an accessible way of forecasting the dynamic market, particularly some of the price movements in the financial market. The results are calculated with R.12